杨文龙 , 杜德斌, 游小珺, 史文天, 颜子明

, 杜德斌, 游小珺, 史文天, 颜子明

华东师范大学城市与区域科学学院/华东师范大学科技创新与发展战略研究中心,上海 200062

Yang Wenlong, Du Debin, You Xiaojun, Shi Wentian, Yan Ziming

中图分类号: K902

文献标识码: A

文章编号: 1000-0690(2017)09-1300-10

通讯作者:

版权声明: 2017 《地理科学》编辑部 本文是开放获取期刊文献,在以下情况下可以自由使用:学术研究、学术交流、科研教学等,但不允许用于商业目的.

基金资助:

作者简介:

作者简介:杨文龙(1991-),男,福建平潭人,博士研究生,主要从事世界地理和创新地理研究。E-mail:yangwenlong_pt@163.com

展开

摘要

基于复杂网络方法,运用GIS、Pajek、Matlab和数据库等技术手段,构建世界跨国投资网络,考察2001~2012年世界跨国投资网络结构及其复杂性的时序演化过程。根据研究可以得出以下主要结论:① 世界跨国投资网络整体遵循“核心-边缘”的圈层结构,结构内部不断变化和重组,呈现由双核主导向多核互联演变,形成资本从西欧、北美、东亚向北欧、南美、西亚、东南亚流动的格局;② 世界投资网络具有显著小世界性质和无标度特征,无标度特征伴随时间的推移趋于弱化;③ 投资活动活跃的国家,对跨国投资网络拥有更强的控制力,但对强化投资的可达性作用不显著,其主要受市场等潜在因素的影响;④ 跨国投资结构的复杂性由高到低依次为中枢型投资地、区域型投资地、一般型投资地、孤立型投资地,不同功能类型的空间分布具有显著的集聚性。

关键词:

Abstract

Using complex network analysis, this study applied GIS, Pajek, Matlab and database, etc., to build the global transnational investment relationship network, and analyzed the temporal evolution of the spatial structure and network complexity of the global transnational investment network from 2001 to 2012. The results shows: 1) The global transnational investment network is showing a “core-edge” ring structure, whose inner structure is changing and reorganizing. The investment network transformed from dual-core (North America and Western Europe) structure into overlapped and related multi-core (North America, Western Europe, the Caribbean, Eastern Asia and Australia) topological structure, with capital gradually flowing from Western Europe, North America, and Eastern Asia to Northern Europe, South America, West Asia and Southeastern Asia in the macroscopic view. 2) The small-world characteristic of the investment network is prominent. The network is scale-free and shows a decrease overtime. 3) The countries that are active in the investment have higher control of the transnational investment network. The confounding factors influence the spatial reachability of the transnational investment. 4) Ranked by the complexity (dissimilarity) of the transnational investment structure, the result from high to low is terminal invest countries, regional invest countries, normal invest countries and isolated investment countries. Countries with different functional types have a clear trend of clustering.

Keywords:

伴随跨国公司扩大在全球范围内生产要素的优化配置[1],资本在国家经济的相互渗透中加速流动,以“资本流”为主体的网络空间应运而生。发达国家与发展中国家的双向直接投资流量不断增长,第三国效应对国家间投资的作用凸显[2~4]。由于全球资源的稀缺性造成全球经济配置的空间依赖性,因此第三市场效应开始对国际经济的供需系统、经济外部集聚效应和溢出效益产生显著影响[5],进而成为投资区位选择以及垂直复合型FDI(Foreign Direct Investment)的重要组成部分[2]。有实证研究发现,荷兰将近一半电子和电气应用行业的外资公司的销售重点不在荷兰[3];爱尔兰、比利时和荷兰在美跨国公司相对较高的销售是在欧盟内部国家[6]。此外,投资枢纽型第三方国家愈发成为跨国公司对外投资的战略选择。多数跨国公司进驻新加坡是基于其邻近东亚、东南亚的区位条件;跨国公司在中国香港和中国台湾的投资偏好是中国大陆的潜在市场;离岸金融中心(offshore financial centre)作为投资的“避税天堂”多邻近发达国家,受跨国资本的青睐;中间产品生产环节也多邻近于发达国家[7]。

垄断优势理论从结构性的市场不完全出发,基于不同企业的特定优势,论述发达国家企业对东道国投资的动因[8, 9]。内部化理论从自然性的市场不完全出发,结合国际分工和企业国际生产的组织形式进行阐释,指出中间产品的不完全性增加了企业的交易成本,使得企业将外部市场内部化,跨国投资行为就是企业超越国家边界的内部化行为[10]。生命周期理论承继垄断优势理论中的特有优势,认为企业跨国投资行为发生在产品成长和成熟阶段,主要是为了规避关税和非关税贸易壁垒[11]。由于发展中国家的生产技术、管理经验、机器设备、营销网络、资本积累等与发达国家存在较大差距,在国际上不具备垄断优势,以垄断优势为主线发展的传统跨国投资理论逐渐失去解释力,随后形成一系列适用于发展中国家跨国投资的理论,如小规模技术理论、技术地方化理论、技术创新产业升级理论等,以及L-L-L(linkage, leverage and learning)范式[13]、制度规避主义[14]。有些学者强调在发展中国家跨国投资过程中,政府发挥着重要的作用,并为了创造独特的战略可能性,运用基于国家专用优势和企业专用优势相互作用的战略[15]。随着中国跨国投资取得引人注目的成绩,国内学界越来越多地从宏观层面关注中国对外直接投资以及利用外资情况[16~18]。地理学者对跨国投资的研究主要侧重于投资行为的空间分异及投资区位的选择差异[1, 20, 21]。综上可见,传统跨国投资理论多忽视第三方国家的关联性影响,实证研究多囿于东道国和母国的二元关系对跨国投资区位选择的决定影响。

然而,传统二元关系逻辑已较难直接解释由区域贸易投资协定勃兴和市场因子波动所引起的整个投资格局变化,无法准确把握双边投资的动力机制[4]。鉴于此,本文引入关系数据构建世界跨国投资网络,结合复杂网络理论从全球层次揭示跨国投资网络的演化趋势,揭示不同区域在投资网络中的功能差异,识别不同国家在跨国投资网络中的位置和功能。一方面,本研究可以为跨国投资系统的网络结构辨识提供崭新的视角,丰富对世界跨国投资一般演化规律和轨迹的认识,拓展跨国投资的实证研究;另一方面,本研究能从世界投资网络透视全球生产网络的运行方式,研判不同国家在生产网络中的角色地位和竞争优势,厘清跨国投资背后的深层含义,对补充和深化跨国投资的理论研究具有重大意义。此外,“一带一路”沿线国家和地区经济发展水平不一、比较优势各异、要素禀赋不同,本研究对“一带一路”沿线国家在跨国投资网络中功能和角色的准确判断,能为中国在“一带一路”对外投资战略的空间差异化选择提供重要的参考价值。

结合网络复杂性的全球经济研究是目前西方世界经济地理研究领域的前沿[22],成为研究全球生产网络和价值链变革的基本单元。国内基于复杂网络方法的研究层出不穷,普遍揭示了国际经济网络是介于规则网络和随机网络间的复杂网络[23~25]。本文选取国家抽象为网络节点,国家之间的投资流抽象为网络连接节点的边,从而构建跨国投资网络。为了客观反映世界跨国投资网络结构的时空演化情况,本文选取2001~2012年世界各国相互投资流量的数据,构建有向加权的投资网络,以测度投资网络中节点(投资国家)和边(国家间投资流)的增减情况,进而研究跨国投资网络结构的演化特征。本研究数据主要来源于联合国贸易与发展会议(UNCTAD)网站中双边外商直接投资的数据库以及《世界投资报告》[26]。

1.2.1 网络结构模型判定

1) 网络密度[d(G)]:描述一个图中各个点之间关联的紧密程度,测量网络图完备性程度。即实际拥有的连线数与最多可能拥有的线数之比:

式中,[o(x)]表示国家x的对外投资总额。网络中节点加权度分布情况用概率分布函数[P(k)]表示。当[P(k)]为幂函数时,指示网络结构具有无标度性质[27]。

2) 加权度(WD):节点加权度定义为在加权网络中与节点连接边的平均权重,均指示国家对外投资活跃程度。公式如下:

网络中节点度或加权度分布情况用概率分布函数

3) 平均路径长度(L):网络的平均路径长度

式中,

4) 簇系数(C):一个节点与其所有邻接点之间连边的数目与可能的最大连接边的数目的比值[28],反映投资网络国家集聚情况的参数。公式如下:

式中,国家

1.2.2 节点的中心性

1) 度中心性(DC):度中心性用节点度的大小进行衡量,可以直观反映该节点与网络中其他节点发生直接联系的可能性大小[29]。节点的度中心性值越大,则国家与其他国家发生投资联系的可能性越大。即

2) 中介中心性(BC):中介中心性用所有节点对间的最短路径经过给定节点的次数和衡量,反映国家在投资网络中的中转和衔接功能[29]。即

3) 邻近中心性(CC):邻近中心性用给定节点到所有节点的最短距离和的大小衡量,反映该国家在投资网络中的相对可达性大小[29]。即

上述3个中心性公式中,n为投资网络中参与的国家数;

1.2.3 结构对等性

对等性分析就是识别那些拥有相似关系模式的行动者,分析这些行动者是否符合特定的角色或者“位置”,或者也可以反过来研究那些处于相似角色或者“位置”的行动者是否会参与典型的关系模式[30],如果相同,则可以划入具有同一意义的类别中。在一个网络关系中,若两个行动者相互替换后没有改变整个网络的结构和性质,可认为二者在结构上是对等的[31]。结构对等性的分析思路与世界跨国投资网络中国家的角色和功能有着较强的共通性。例如,在衡量两个国家角色和功能是否相同时,不仅要求两个国家对外投资和国内外商投资的国家数目基本相同,更要求其与相同的核心投资国连接,并控制着同样的投资边缘国。因此,本文借用社会网络分析方法中的结构对等性分析法,以找出投资网络结构中国家投资结构相同(相似),角色或位置相当的国家,并揭示其功能类型意义,具体的方法运用层次聚类算法,通过专业软件Pajek实现[32]。

随着国际化深入发展,越来越多国家被嵌入全球价值链中,参与全球生产分工体系,推动着国际产品由“一国制造”转向“世界制造”。世界投资规模总体波动上升,网络呈现稠密化趋势。2001~2012年,投资网络节点数由183个增加至189个;节点平均度由8.39增加至12.14;边数由1 543条增加至2 306条,增长了1.49倍;平均加权度由42.79增长至108.16,增长了2.53倍;密度由0.05增长至0.06(表1)。2008年的金融危机是世界投资再配置的重要转折,网络特征统计量均在2008年前后达到峰值,尤其边数和平均加权度在2008年后出现不同程度的下降。一是受金融危机引发跨国公司“撤资潮”的影响,跨国公司为偿还母公司债务,撤回公司内部贷款和抽回投资,主要发生在发达国家。二是受金融危机导致金融市场萎缩和跨国公司资金短缺的影响,全球跨国并购大幅减少。

表1 2001~2012年世界跨国投资网络的特征量统计

Table 1 The features of the global transnational investment network in 2001-2012

| 节点数 | 边数 | 平均度 | 平均加 权度 | 网络 密度 | 簇系数 (C) | 平均路 径长度(L) | |

|---|---|---|---|---|---|---|---|

| 2001 | 183 | 1543 | 8.39 | 4279.45 | 0.05 | 0.39 | 2.37 |

| 2002 | 187 | 1599 | 8.55 | 3956.25 | 0.05 | 0.36 | 2.35 |

| 2003 | 191 | 1763 | 9.23 | 3946.17 | 0.05 | 0.39 | 2.40 |

| 2004 | 195 | 2016 | 10.34 | 4999.03 | 0.05 | 0.46 | 2.29 |

| 2005 | 199 | 1732 | 8.70 | 5749.35 | 0.04 | 0.31 | 2.11 |

| 2006 | 197 | 2354 | 11.95 | 7601.57 | 0.06 | 0.50 | 2.28 |

| 2007 | 196 | 2555 | 13.04 | 12232.68 | 0.07 | 0.52 | 2.27 |

| 2008 | 199 | 2610 | 13.12 | 11125.32 | 0.07 | 0.48 | 2.24 |

| 2009 | 195 | 2427 | 12.45 | 8229.03 | 0.06 | 0.50 | 2.27 |

| 2010 | 204 | 2477 | 12.14 | 8619.23 | 0.06 | 0.45 | 2.32 |

| 2011 | 201 | 2499 | 12.43 | 10421.30 | 0.06 | 0.48 | 2.29 |

| 2012 | 189 | 2306 | 12.14 | 10815.63 | 0.06 | 0.45 | 2.33 |

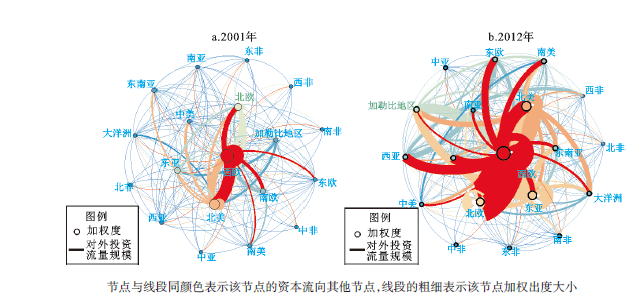

跨国投资网络整体遵循“核心-边缘”结构,核心区与边缘区的国家伴随着内部特征的变化和重组而出现更迭。西欧和北美稳居跨国投资网络的核心,东亚地区后来居上,南欧逐渐退出次核心地位(图1)。2001年和2012年,西欧和北美对跨国投资流量之和占全球跨国投资流量的比例为53.91%和43.31%。东亚、北欧和加勒比地区则处于第二层级,2001和2012年对外直接投资流量和国内外商直接投资流量的总和占全球投资流量的比例依次为7.63%和10.46%、14.02%和13.82%、4.67%和6.30%。主要由于西欧和北美处于全球价值链上游,在世界生产分工体系中居于支配地位,跨国投资规模远超其他地区;东亚国家受金融危机冲击小以及全球投资资源再分配的影响,经济水平与北美、西欧的差距缩小,逐步跻身投资网络的核心地位;南欧国家由于产业结构低等级性,在遭受欧债危机的冲击后,对外投资规模缩小,外商直接投资吸引力大幅减弱。

资本由西欧、加勒比、南欧向北美、中美、南美流动逐渐演变为由西欧、北美、东亚向北欧、南美、西亚、东南亚流动。2001年,西欧、加勒比、南欧加权入度与加权出度的差值依次为-56 416、

-31 717、-21 637,北美、中美、南美加权入度与加权出度的差值依次为37 390、25 555、19 740。2012年,西欧、北美、东亚加权入度与加权出度的差值依次为-226 809、-214 050、-86 803;北欧、南美、西亚、东南亚加权入度与加权出度的差值依次为243 727、67 630、67 417、33 668。主要原因包括:① 采掘业的发展带来跨国投资的资源吸引,市场拓展带来跨国投资的空间吸引,南美和西亚吸引了大量外资流入;② 发达国家间的跨国并购大幅缩减,以发展中国家为主导的跨国并购迅速增长,主要集中于西亚、南美、东南亚;③ 在西亚、南美、东南亚的“绿地投资”增长更胜于跨国并购,如在巴西、约旦、缅甸和越南等国家的投资[33]。

2001年,世界跨国投资网络呈双核主导,美国与西欧的德国、英国、法国、卢森堡相互投资占重要比重,西欧区域内部投资形成次一级投资网络,西欧与东亚的投资次网络初现端倪(图2)。该时期,美国和西欧等发达国家之间相互投资是世界投资的普遍现象,投资规模大,产业多为双方比较优势产业;卢森堡虽为小国,但其作为世界第二大基金投资中心、第七大金融中心,凭借稳定的经济、社会和政治局势,银行保密制度和投资商保护、高素质和国际思维的劳动力,以及居欧洲中心的区位优势,成为欧洲最受欢迎离岸公司国家[34]。2012年,跨国投资网络的复杂特性整体涌现,逐渐形成多核心交叉联系的拓扑结构(图2),五大核心区分别由北美的美国;加勒比地区的英属维京群岛、开曼群岛等;西欧的德国、英国、法国、卢森堡、比利时、荷兰等;东亚的中国、中国香港、韩国、日本以及大洋洲的澳大利亚等国家和地区构成。北美和西欧对拉美、非洲和中东欧等外围区域的投资构成次一级网络。一方面,与2001年相比,2012年美国从节点最大的国家急剧缩小,但其与其他国家地区的联系强度却显著增加,除了增强原先与西欧的联系之外,美国与澳大利亚、新加坡、中国的投资联系也增强。另一方面,世界投资网络增加了许多新节点,南美洲的内部联系和对外联系增加、南非与西欧联系增加、澳大利亚对外联系增加。

图1 2001和2012年世界跨国投资网络的拓扑结构

Fig. 1 The topological structure of the global transnational investment network in 2001 and 2012

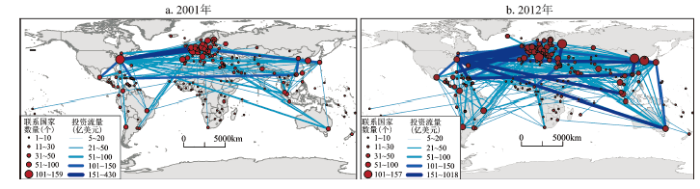

图2 2001和2012年世界跨国投资网络的空间格局

Fig. 2 The spatial pattern of the global transnational investment network in 2001 and 2012

2001~2012年,投资网络各年份的平均最短路径(L)在区间2.11~2.40,均略低于相同节点和边数的随机网络平均路径长度理论值(L′)(2.33~2.67);簇系数(C)在区间0.31~0.52,远高于随机网络聚类系数(C′)(0.04~0.07)(表1)。这一结果表明了跨国投资网络的小世界特征显著。区域内的跨国投资可以使生产从自给自足向小范围分工跃迁,区域间的跨国投资使世界出现产业集聚和全球分工,这种更大范围的分工体系和生产网络未导致世界投资凝聚力的下降,而世界投资网络仍呈现小世界的特征,而且“小世界”形态的投资网络具有较高的投资效率。因为网络是全连通的,因此可以在全局网络中实现帕累托(Pareto)改进,可以促进世界生产分工的深化和细化。

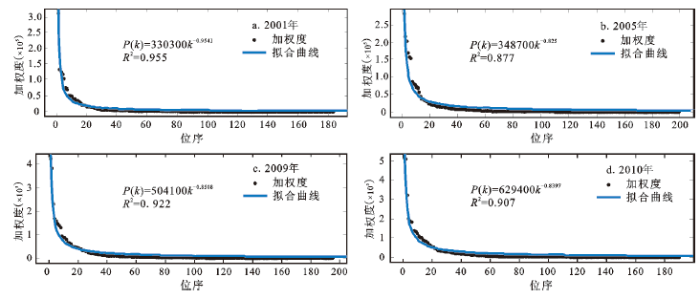

跨国投资网络加权度分布遵从典型的长尾分布,服从无标度特征。网络的加权度与幂函数拟合的相关系数基本保持在0.9,最高可达0.955,表现为极显著,呈现幂律分布特征,具有明显的“富人俱乐部”现象(图3)。2001年,排名前20%的节点拥有95.93%的加权度;2005年该比例下降至93.24%;2009年该比例进一步下降至92.01%;2012年维持在92.06%。2001、2005、2009和2012年的指数参数依次为-0.954、-0.825、-0.851和-0.831,呈减小趋势,说明跨国投资网络的无标度特征不断弱化,投资流量规模变差正在缩小,中间位序的地区单元数增多,也指示了全球投资网络结构不断优化,降低投资权力过度集中于某些国家或地区所导致投资网络的不稳定性。出现该变化特征的原因在于跨国投资网络的择优选择机制在金融危机后未完全发挥作用。择优连接和增长性是跨国投资网络生产无标度的两个基础,金融危机造成美国和西欧国家跨国投资的活跃度下降,母国不是在网络中寻找投资连通度大的国家进行投资,而是选择受金融危机冲击较小且具有要素低成本吸引力的东南亚国家进行投资。

图3 2001~2012年世界跨国投资网络加权度分布

Fig. 3 The weighted degree distribution of the global transnational investment network in 2001-2012

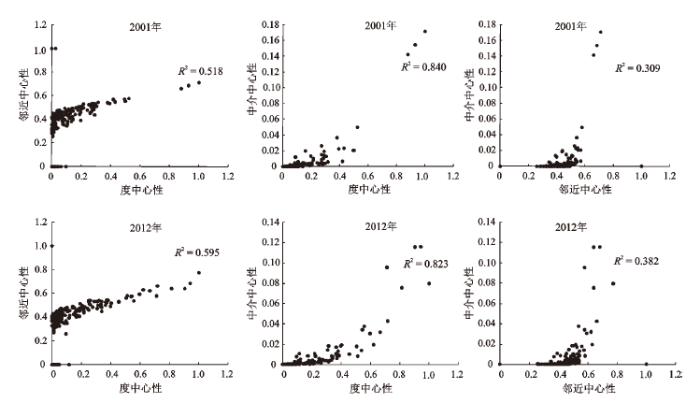

度中心性、中介中心性和邻近中心性的相关程度具有良好的时间惯性。2001和2012年,度中心性与邻近中心性的相关系数分别为0.518和0.595;度中心性和中介中心性的相关系数分别为0.840和0.823;邻近中心性和中介中心性的相关系数分别为0.309和0.382(图4)。度中心性与邻近中心性、中介中心性具有较高的关联性。2001和2012年度中心性与中介中心性关联性均高于0.8,表明在投资网络中投资活动活跃的国家具备在该网络中的“掮客”、中转的功能,对跨国投资网络拥有更强的控制力。2001和2012年度中心性与中介中心性关联性也为正,但相关系数不大(0.5~0.6),这表明一个国家投资吸引力还受市场、资源、要素成本、政策优惠等因素影响,不是所有对外投资规模大、投资伙伴多的国家,都具有较高的空间可达性。邻近中心性与中介中心性的相关性不显著,表明了空间可达性较高的国家不具备对投资网络的控制优势。

图4 2001年和2012年投资网络节点度中心性、邻近中心性和中介中心性的相关性

Fig. 4 The corelation among Degree Centrality, Closeness Centrality and Betweeness Centrality of the nodes in the investment network in 2001 and 2012

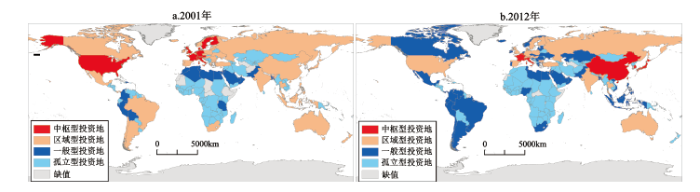

运用层次聚类法,考察国家在投资网络中的结构对等性,以揭示国家在投资网络中的地位及行动者角色。将国家分成4种功能类型(图5):① 中枢型投资地;② 区域型投资地;③ 一般型投资地;④ 孤立型投资地。随着时间推移,4种功能类型的空间分布格局存在不同程度的变化。

图5 2001和2012年投资地功能类型的空间格局

Fig. 5 The spatial pattern of the investment functional types in 2001 and 2012

1) 中枢型投资地。该功能类型的国家在世界跨国投资网络中有较高的活跃度,并且处于投资网络的结构洞位置,控制网络的投资资源。该地区的国家与世界其他多数国家均保持直接的投资互动关系,联系畅通,跨国公司大多在该地区国家进行投资,进而实现资金、商品、信息、技术等要素在全球的扩散和集聚,提升跨国公司对世界投资资源的控制力。2001年,世界投资仍以西方国家为主导,具有该功能类型的国家集中分布在北美、西欧、北欧等发达国家,包括美国、德国、法国、瑞典、瑞士、荷兰、意大利、英国、奥地利、芬兰、丹麦,投资结构的非相似性值为0.72。2012年,国家数量减少至7个,集中于东亚等新兴国家以及少数西欧发达国家,包括卢森堡、比利时、意大利、法国、中国、日本、韩国,投资结构的非相似性也减少为0.51,表明中枢型投资地的国家投资结构趋于同质化,投资形式的多样性减小。

2) 区域型投资地。该功能类型拥有较强的结构洞功能,是投资流进入中枢型投资地的主要通道,是各自区域投资资源的集散地。虽然该地区的国家在投资结构中的终点投资地作用有限,但在世界投资发展中有着举足轻重的作用,一方面与中枢型投资地保持着紧密的投资联系,另一方面将承接的商品流、资金流、信息流等辐散到其他国家,是不同区域投资流集聚和扩散的中心。这种类型的国家多集聚着垂直复合型FDI,在全球生产网络中承担中间环节产品的生产和转出口的平台。2001年国家数量为49个,主要包括韩国、日本、新加坡、中国、中国台湾、中国香港、印度、加拿大、泰国等国家或地区,集中分布在新兴国家或地区。投资结构的非相似性为0.49,低于同时期中枢型投资地的结构非相似性。2012年国家的数量同样呈现减少的特征,减至20个,主要包括印度、新加坡、中国台湾、英国、德国、丹麦、美国、瑞士、俄罗斯等国家和地区。德国、英国、美国、澳大利亚等发达国家表现出投资功能由中枢型向区域型的功能转变,原因在于这些国家在金融危机后投资活跃程度减弱,择优选择机制未完全发挥。该时期的投资结构非相似性为0.46。

3) 一般型投资地。该功能类型的投资活跃程度和中介中心性均处于或略低于平均值。共同特征是彼此间的投资联系较少,投资流主要集中在它们与上述两类投资地的联系,以外商直接投资为主,主要依托中枢型投资地、区域型投资地对其投资的渗透带动。2001年,国家的数量为26个,主要分布在中东、北非、南美地区,结构非相似性为0.22。2012年,国家数量增长为58个,仍集中分布在北非、西亚和南美地区,结构非相似性也增加至0.78。这些国家的共同特点是产业结构单一、以能源出口为导向,其传统能源供应基本为西方跨国公司垄断,非传统和新资源也发展成跨国公司投资的富集区,因此具有相对较低的投资结构复杂性。

4) 孤立型投资地。该功能类型的特征是各项中心性指标普遍较低,内外投资流量稀少,只依靠与少数国家或地区之间的投资流联系,如果仅有的几个投资通道被隔断,其就会成为世界投资网络孤立点,独立于整个投资网络之外。该地区整体上是世界跨国投资“冷区”,对外投资能力有限,仍以外商直接投资为主。2001年,国家数量为97个,集中分布在非洲、西亚地区,结构非相似性为0.12。2012年,国家略微增加至109个,仍主要集中于非洲、西亚地区,结构非相似性略上升至0.29。该功能类型分布地区多为第三世界的国家,缺乏对世界资本的吸引力,在世界投资市场作用相对较弱,处于投资网络的边缘位置。由于该功能类型的国家与其他国家的投资联系少,投资结构单一,因此具有最低的非相似性。

综上可得,随着不同区域在世界投资网络中功能性等级下降,跨国投资结构的复杂性(非相似性)减弱,不同功能类型国家的分布具有显著的集聚特征,中枢型投资地与区域型投资地存在高度空间集聚性,一般型投资地与孤立型投资地在空间上也趋于集聚。

突破二元关系的传统视角对跨国投资的研究惯性,构建世界跨国投资网络,从整体剖析网络的拓扑结构及其演化规律,基于复杂网络理论考察网络的复杂性,研究结果如下。

1) 投资网络呈现“核心-边缘”的圈层结构,西欧和北美国家仍在世界跨国投资网络中占据主导。虽然新兴经济体跨国投资的迅猛发展,发展中国家和发达国家跨国投资规模差距缩小,使核心区和边缘区的国家出现更迭,但仍未能改变网络“核心-边缘”特征。美国次贷危机和欧洲债务危机成为全球投资资源再分配的重要转折,欧洲和北美国家跨国投资下降明显,亚洲、南美洲和加勒比地区上升至历史高位。一方面由于欧美国家和地区的财政赤字、债务危机、失业率增加等矛盾,导致跨国公司的投资信心下降,严重降低了西欧和北美之间的投资规模。另一方面东南亚、南美洲、加勒比地区和东亚的劳动力、资源、新兴产业、优惠政策和市场等优势,扩大对外开放,促进跨国投资的便利化,为跨国公司投资提供有利条件。

2) 投资网络趋于稠密化发展,网络整体复杂性涌现,拓扑结构由双核(北美和西欧)主导向多核(北美、西欧、加勒比地区、东亚和大洋洲)互联演化,世界经济逐渐形成资本从西欧、北美、东亚向北欧、南美、西亚、东南亚流动的宏观格局。其变化的机制主要包括4个方面:① 经济发展推动。后金融危机,新兴国家经济(尤其“金砖五国”)的经济增长相对稳定,发达国家经济增速滑落,呈现东强西弱的变化特征。东亚经济复兴(尤其中国崛起)改变了东亚整体产业结构,促进垄断竞争优势的形成,为跨国投资提供条件。② 技术升级带动。虽然东亚(尤其中国)丧失了人口红利和成本优势,全球对东亚的投资驱动力减弱,但技术的本土化和创新带来国际垄断的相对优势,东亚对外投资规模不断增加。③ 成本优势拉动。北美和西欧的跨国投资对东南亚低要素成本产生吸引,东南亚外商直接投资规模日益提高,东南亚成为全球资本流入的热点区。④ 优惠政策驱动。税收等优惠政策对于危机后发达国家外资吸引作用显著,离岸金融中心和特殊目的公司的跨境投资活跃,如卢森堡、比利时、荷兰和爱尔兰4个小国,投资者(尤其SPEs)在这些国家能享受较低税率。加勒比地区的英属维京群岛、开曼群岛也成为跨境资本的集中营,成为发展中国家资本进入北美的重要通道。

3) 投资网络具有显著的小世界特征,全球生产网络和分工体系增强了世界投资的凝聚性,“小世界”形态的投资网络进一步促进了世界生产分工的深化和细化;跨国投资网络服从无标度特征,择优选择机制和增长性诱发了跨国投资网络的“富人俱乐部”现象,但随着金融危机缩小了发达国家和发展中国家的投资差距,择优选择未能得以完全发挥,投资网络的无标度特征趋于弱化;不同中心性指标之间的相关性分析显示投资网络中投资活动活跃的国家,对跨国投资网络拥有更强的控制力,而跨国投资的空间可达性不完全由投资规模和投资伙伴数量决定,还受到市场、资源、要素成本、政策优惠等其他潜在因素的影响。

4) 跨国投资是国家经济水平、产业优势、区位优势、要素禀赋、政策优惠等众多因素共同作用的结果,国家在投资网络中的功能角色也受制于此。其中,经济水平、产业优势、区位优势的影响更为显著。① 中枢型投资地主要分布在发达国家,这些国家的资本、技术、管理、规模经济等在国际具备垄断优势,跨国投资以市场驱动和垄断优势驱动,对外投资空间无远弗届,对外投资产业复杂多元,因此具有最高的结构复杂性。② 区域型投资地多分布在新兴国家,还有一部分分布在离岸金融中心,与中枢型投资地的国家邻近。新兴国家投资遵循“由近及远”和“经济水平相近原则”,对外投资多从周边国家或地区向外辐射,成为各自区域的投资集散地。新兴国家在国际上虽不具备垄断优势,但一方面要素成本低廉,能够获得相对的比较区位优势;另一方面小规模生产技术和技术地方化在国际上具有优势。离岸金融中心凭借邻近发达国家的优势以及优惠的税收政策吸引大量外资。③ 一般型投资地多为资源型国家,跨国投资多为资源驱动型投资,投资结构单一,投资结构复杂性相对较低。④ 孤立型投资地多为第三世界国家,集中分布在非洲和西亚,这些国家不具备上述因子的相对优势,因此与其他国家建立的投资关系少,对外投资规模小,基本处于投资网络的边缘位置。

5) “一带一路”沿线国家横贯东南亚、南亚、中亚、西亚和中东欧国家,多为跨国投资“冷区”。其中,东南亚、西亚和中东欧国家在跨国投资网络中多为一般型投资地,中亚和南亚(除印度和巴基斯坦)的国家多为边缘型投资地。基于“边际扩张理论”,中国应加强对这些地区的产业梯度转移。① 中国-东盟的合作框架和区位邻近优势促进中国对东南亚的投资便利化。中国宜利用东南亚劳动成本优势,加快制鞋和服装等劳动密集型产业在该地区的投资。② 中亚国家工业化水平较低,基础设施建设将是未来一段时期的发展重点,一定程度上带动钢铁产品需求大幅增长。同时,该地区的国家拥有相对丰富的矿产资源,中国宜加大该地区钢铁业的投资力度。③ 中亚和西亚国家多是油气资源的富集区,中国宜在该地区加强石油、天然气等领域的投资。④ 中东欧国家相对“一带一路”沿线其它国家在跨国投资网络中具有更高的功能性,区位条件优越,邻近西欧和北欧等发达国家,同时具有较强的工业基础和专业技术,中国可发挥其基础设施建设、装备制造业的相对优势,加强装备制造、高铁建设以及新能源开发等领域的投资。

投资区位选择的战略决策不仅受双边国家的经济条件、资源禀赋、政策环境、制度设置等内生变量的作用,同时受邻近国家在投资网络中的位置和功能的影响,具有空间依赖性。在今后的研究中,对于国家在跨国投资网络中的外部影响因子以及投资网络的动力机制仍需深入探讨。

The authors have declared that no competing interests exist.

| [1] |

跨国公司R&D全球化: 地理学的视角 [J].R&D globalization by MNCs: A perspective from geography. |

| [2] |

Beyond trade: The impact of preferential trade agreements on FDI inflows [J].https://doi.org/10.1016/j.worlddev.2011.04.036 URL [本文引用: 2] 摘要

This paper investigates the effects of preferential trade agreements (PTAs) on net FDI inflows of member countries using a comprehensive database of PTAs in a panel setting. PTA membership is associated with a positive change in net FDI inflows and FDI gains increase with the market size of PTA partners and their proximity to the host country. The estimated relationship is driven by the developing countries in the sample and agreements signed in the late 1990s–early 2000s, a period when the majority of “deep integration” PTAs have been advanced.

|

| [3] |

Kranenburg H L V. Roles of foreign owned subsidiaries in a small economy [J].https://doi.org/10.1016/j.ibusrev.2005.09.005 URL [本文引用: 1] 摘要

This study explores the roles and characteristics of foreign owned subsidiaries in a small economy within a trading block. Four role types of foreign owned subsidiaries are identified: local satellite, truncated miniature replica, export platform, and the regional or world mandated hub. Evidence is provided on the sales focus of foreign owned subsidiaries in the Dutch electronics and electrical applications industry. We find that almost half of the foreign owned subsidiaries focus their sales on more markets than just the Netherlands. These subsidiaries use the Netherlands as an export base. They supply the European market with products that are produced in one location, instead of using multiple production plants. The results show that these subsidiaries with a non-European parent are relatively young and focus also on manufacturing activities.

|

| [4] |

Estimating regional trade agreement effects on FDI in an interdependent world [J].https://doi.org/10.1016/j.jeconom.2008.05.017 URL [本文引用: 2] 摘要

Recent research on trade and multinationals highlights that multinational firms- integration strategies are complex and the degree of vertical integration varies in a multilateral world with many possible locations of activity. In particular, multinationals control a large fraction of trade within the block of developed countries. The most important regional trade agreements (RTAs) are signed between members of the very same block of economies. This gives rise to the question asked in the present paper: what is the impact of RTAs on FDI in an interdependent world? Recent spatial HAC estimation techniques are applied to both estimation and testing.

|

| [5] |

Waddell G R et al. FDI in space: Spatial autoregressive relationships in foreign direct investment [J].https://doi.org/10.1016/j.euroecorev.2006.08.006 URL [本文引用: 1] 摘要

There are a number of theoretical reasons why foreign direct investment (FDI) into a host country may depend on the FDI in proximate countries. Such spatial interdependence has been largely ignored by the empirical FDI literature, with only a couple recent papers accounting for such issues in their estimation. This paper conducts a general examination of spatial interactions in empirical FDI models using data on US outbound FDI activity. We find that estimated relationships of traditional determinants of FDI are surprisingly robust to inclusion of terms to capture spatial interdependence, even though such interdependence is estimated to be significant. However, we find that both the traditional determinants of FDI and the estimated spatial interdependence are quite sensitive to the sample of countries one examines.

|

| [6] |

Export-platform foreign direct investment [J].https://doi.org/10.2139/ssrn.739213 URL [本文引用: 1] 摘要

A poorly understood empirical phenomenon is export-platform affiliate production (EP), particularly for sale in third countries rather than in the parent or host countries. We develop a three-region model, with two identical large, high-cost countries (collectively called North) and a small, low-cost country (South). The large countries each have one firm. Our theory section analyzes the conditions under which one or both of these firms uses the South to produce for (a) export back to the parent (home-country EP), (b) export to the other large country (third-country EP), or (c) export to both (global EP). A free-trade area between one of the northern countries and South can lead to the insider northern firm choosing home or global EP and the outsider firm choosing third-country EP for a range of parameter values. Our empirical section shows the relevance of this outcome. Foreign manufacturing affiliates of US multinationals inside North America concentrate on home-country EP while affiliates inside Europe concentrate on third-country EP.

|

| [7] |

Economic integration within Greater China: Trade and investment flows between China, Hong Kong and Taiwan [J].https://doi.org/10.1017/S0305741000032318 URL [本文引用: 1] 摘要

Economic integration is essentially a process of unification - the means whereby coherence is imposed upon previously separate, even disparate, geographical regions. It may be pursued as a domestic or international goal, although the simultaneous attainment of both may prove elusive. Recent efforts towards the creation of formal trans-national, regional economic identities, whether North American (NAFTA), European (EC) or Asian-Pacific (APEC), have sometimes been perceived as a threat to the establishment of a truly integratedglobaleconomy. By contrast, the remarkable degree of economic integration already achieved between southern China and Hong Kong (and, latterly, Taiwan) might ironically have a fissiparous effect on China'sdomesticeconomy. From this point of view, there is a danger that increasing economic integration within Greater China could threaten China's national economic identity, or at least compel its re-definition.

|

| [8] |

The international operations of national firms: A study of direct foreign investment [J].https://doi.org/10.1007/978-1-137-28787-8_10 URL [本文引用: 1] 摘要

react-text: 479 L'objectif de ce travail est d'étudier le comportement informationnel des entreprises interna-tionales et en particulier les pratiques d'intelligence économique (IE) menées par les PME exportatrices. Il vise particulièrement à caractériser les activités des PME exportatrices en ma-tière de recherche de l'information, de protection de leur patrimoine informationnel et d'in-fluence sur leur... /react-text react-text: 480 /react-text [Show full abstract]

|

| [9] |

Dominance and Leadership in the International Economy Exploitation, Public Goods, and Free Rides [J].https://doi.org/10.2307/2600355 URL [本文引用: 1] 摘要

It is often difficult to distinguish dominance from leadership in international economic relations. The latter concept, however, rejects exploitation and implies an often critical function in the provision of public goods. In its absence, the provision of such public goods as a market for distress goods, a steady flow of capital, and a rediscount mechanism may disappear. This stabilization function was provided by the United States in the first postwar decades, but the U.S. now has neither the will nor the international acceptance to play such a role. And a successor is not in sight.

|

| [10] |

The internalisation theory of the multinational enterprise: A review of the progress of a research agenda after 30 years [J].https://doi.org/10.1057/jibs.2009.49 URL [本文引用: 1] 摘要

This paper reviews the progress of the research agenda initiated by The Future of the Multinational Enterprise (1976). Focusing initially on the problem of explaining the existence of the multinational enterprise, the agenda soon broadened to encompass the analysis of alternative modes of foreign market entry, the role of international joint ventures, the impact of innovation on corporate growth, and the role of culture in international business. The core philosophy – based on the Coasian nature of the firm and on rational action modelling – has remained constant, while the widening range of applications has encouraged synthesis with theories developed in other fields of research. Success in answering any one question invariably generates new questions, which must in turn be answered through a further extension of the theory, and this dynamic continues to drive the development of the theory today. Internalisation theory has retained its validity and its vitality over the past 30 years, and is currently being extended into new fields of international business research.

|

| [11] |

International investment and international trade in the product cycle [J].https://doi.org/10.1002/tie.5060080409 URL [本文引用: 1] 摘要

Location of new products, 191.--The maturing product, 196.--The standardized product, 202.

|

| [12] |

The determinants of international production [J].https://doi.org/10.1177/2325967113497189 URL 摘要

No abstract is available for this item.

|

| [13] |

The international entrepreneurial dynamics of accelerated internationalization [J].https://doi.org/10.1057/palgrave.jibs.8400271 URL [本文引用: 1] 摘要

The initial stages of internationalisation, prior to firms having established their definitive sources of advantage, remain the relatively unexplored area of the international business (IB) literature. At these early stages, where firms are seeking to establish themselves, and new multinational firms are appearing to exploit new opportunities created by globalisation, the entrepreneurial aspects of internationalisation come to the fore. In this paper we aim to delineate an emerging field of IB scholarship: we use the appearance of international new ventures, and the phenomenon of accelerated internationalisation that they feature, to identify a set of issues that has slipped through the net of some of the existing IB frameworks. We propose that the salient features of accelerated and early internationalisation by the newly internationalising firm are best captured in a framework that is found at the intersection of entrepreneurial and internationalisation perspectives, which we propose be known as international entrepreneurial dynamics. We discuss such a framework in terms of entry points and pathways mapped by firms as they probe the IB arena, and the key factors that impinge on behaviour and strategic choices. In line with recent developments in the entrepreneurship literature, these are grouped into three milestones of entrepreneurial processes that extend across national boundaries: (1) the discovery of new opportunities; (2) the deployment of resources in the exploitation of these opportunities; and (3) the engagement with competitors. Implications for MNE and internationalisation theory are discussed.

|

| [14] |

Outward foreign direct investment as escape response to home country institutional constraints [J].https://doi.org/10.1057/palgrave.jibs.8400285 URL [本文引用: 1] 摘要

In this perspective paper we argue that outward foreign direct investment (OFDI) undertaken as escape response to perceived misalignment between firm needs and home country institutional conditions represents an important but under-explored phenomenon in the international business (IB) literature. We propose that, in advanced industrialized nations, the extent of OFDI as escape is likely to rise with the extent of societal coordination in the political economy. Societal coordination is associated with relatively slower rates of institutional adjustment and thus with relatively greater prevalence of misalignments that may drive OFDI. We illustrate the face validity of our argument and lay out the implications for future research in IB.

|

| [15] |

Reconciling internalization theory and the eclectic paradigm [J].https://doi.org/10.1108/1525383X201000007 URL [本文引用: 1] 摘要

The eclectic paradigm of Dunning (1980) (with its OLI and four motives for FDI framework) can be reconciled with the firm and country matrix of Rugman (1981). However, the fit is not perfect. The main reason for misalignment is that Dunning is focused upon outward FDI into host economies, whereas Rugman's matrix is for firm-level strategy covering MNE activity in both home and host countries.

|

| [16] |

全球化背景下我国企业对外直接投资的动因研究 [J].A study of the FDI motives of the enterprises of our country under the background of globalization. |

| [17] |

中国对外直接投资的动因 [J].Motives of China’s FDI. |

| [18] |

中国企业对外直接投资动因 [J].The motivation of Chinese enterprises’ foreign direct investment. |

| [19] |

中国吸收外资30年:利用全球资源促进增长与升级 [J].China’s foreign direct investment 30 years: the use of global resources to promote growth and upgrading. |

| [20] |

跨国R&D投资的宏观区位选择 [J].Study on the macro-location choice of overseas R&D by multinational corporations. |

| [21] |

跨国公司功能区位实证研究 [J].Geography of multinational corporations in China: an empirical study of fortune global 500 multinational corporations in electronics and medical and chemical industries. |

| [22] |

Sectoral differentiation and network structure within contemporary worldwide corporate networks [J].https://doi.org/10.1111/j.1944-8287.2011.01122.x URL [本文引用: 1] 摘要

This article contributes to the converging literatures on global production networks and new regionalism, which show that these two entities and their respective geographic scales are complexly interdependent. It explores two key conceptual differences between the leading world city network studies of Alderson and Beckfield and the work of the Global and World City (GaWC) Research Network. The first is the sectoral differentiation of the data, in which the former focuses on multinational corporations in all industrial sectors and the latter specifically targets only advanced producer services. The second involves methodological differences that lead to dissimilar network structures. Alderson and Beckfield made only a basic hierarchical differentiation of the firms, while the GaWC study used a more elaborate classification method. Combining these approaches, we explore firms' global and regional interdependencies (their centrality within their network and its structure). Using a single data set of the top 100 global multinationals (2005) and their ownership linkages with thousands of subsidiaries in 2,259 unique cities worldwide. The findings not only reveal the nodal centralities and linkage structures within the “all industrial sector” network and the “producer service sector” network but also show a strong correlation between these two networks, specifically toward the apex of the economic systems, and evidence of the coexistence of hierarchical and heterarchical city network structures.

|

| [23] |

复杂网络理论下世界原油贸易空间格局演进研究 [J].

依据世界原油贸易数据,以复杂网络理论为基础,结合地理学的区域分析方法,勾勒出世界原油贸易空间结构,并比较了区域间节点、出、入度及权重值的差异。利用熵值分析了网络的均质性,并对世界原油贸易空间结构进行了模拟。研究表明:①尽管世界原油贸易空间格局的节点增幅不大,但随时间推移,节点的度与权重值大幅增加,即世界原油贸易范围及效应在逐渐加大;②通过对节点、出、入度及权重值的比较,揭示了不同区域在世界原油贸易空间格局中的职能差异;③结构熵、权重熵的测定与世界原油贸易空间格局的模拟均表明世界原油贸易空间格局网络的有序性,世界原油空间格局是非均质的。多元化不等于均质化,贸易主体要依据各自所面临的客观环境选择适合区域合作伙伴,才能更好的落实多元化进口策略,切实解决可能面临的石油供给危机。

Evolution of spatial pattern of world crude oil trade based on complicated network theory.

依据世界原油贸易数据,以复杂网络理论为基础,结合地理学的区域分析方法,勾勒出世界原油贸易空间结构,并比较了区域间节点、出、入度及权重值的差异。利用熵值分析了网络的均质性,并对世界原油贸易空间结构进行了模拟。研究表明:①尽管世界原油贸易空间格局的节点增幅不大,但随时间推移,节点的度与权重值大幅增加,即世界原油贸易范围及效应在逐渐加大;②通过对节点、出、入度及权重值的比较,揭示了不同区域在世界原油贸易空间格局中的职能差异;③结构熵、权重熵的测定与世界原油贸易空间格局的模拟均表明世界原油贸易空间格局网络的有序性,世界原油空间格局是非均质的。多元化不等于均质化,贸易主体要依据各自所面临的客观环境选择适合区域合作伙伴,才能更好的落实多元化进口策略,切实解决可能面临的石油供给危机。

|

| [24] |

基于复杂网络的国际铜矿石贸易格局 [J].Hao Xiaoqing et al. International copper ore trade pattern based on complex network theory. |

| [25] |

国际贸易网络拓扑结构的演化 [J].https://doi.org/10.3321/j.issn:1000-6788.2008.10.010 URL [本文引用: 1] 摘要

应用复杂网络方法,研究了1950~2000年间国际贸易网络度分布,群聚性,度相关性和互惠性等拓扑结构特征的演化规律.研究结果表明国际贸易网络不是典型的无标度网络,拓扑结构的异质性在演化过程中不断下降.随着更多国家参与到国际贸易体系中,各国在全球贸易格局中的分工合作日益有序,贸易全球化和区域经济一体化并存的趋势不断加强.

Topological structure evolution of world trade network. Systems Engineering-Theory & https://doi.org/10.3321/j.issn:1000-6788.2008.10.010 URL [本文引用: 1] 摘要

应用复杂网络方法,研究了1950~2000年间国际贸易网络度分布,群聚性,度相关性和互惠性等拓扑结构特征的演化规律.研究结果表明国际贸易网络不是典型的无标度网络,拓扑结构的异质性在演化过程中不断下降.随着更多国家参与到国际贸易体系中,各国在全球贸易格局中的分工合作日益有序,贸易全球化和区域经济一体化并存的趋势不断加强.

|

| [26] |

UNCTAD. World investment report 2001-2012 [R/OL]. |

| [27] |

The structure and function of complex networks [J]. |

| [28] |

Collective dynamics of “small-world” networks [J].https://doi.org/10.1038/30918 URL [本文引用: 2] |

| [29] |

海航航空网络空间复杂性及演化研究 [J].https://doi.org/10.11821/dlyj201405011 URL [本文引用: 3] 摘要

随着民航业市场改革的推进,航空企业逐渐成为影响我国航空网络最为活跃的主体。海航航空是我国最大的股份制航空企业,其网络的空间结构和演化具有一定的典型性。因此,本文以海航航空为例,采用拓扑网络和复杂网络的相关指标,分析海航航空网络的空间结构及其演化特征。研究发现:海航航空网络仍处在不断的发展中,并逐渐呈现出小世界和无标度的特征;节点的中心性间具有较高的相关性,且介中心性位序-规模的变化速率要明显快于度中心性和邻近中心性;网络的中心性处于下降趋势,即网络内部节点的差异逐步减小;海航航空的枢纽选择从地方逐渐扩展到全国,并已基本形成了以北京、西安和海口为核心的网络结构,而其他层级结构尚不明显。

Spatial structure and evolution of Hainan Airlines network: an analysis of complex network. https://doi.org/10.11821/dlyj201405011 URL [本文引用: 3] 摘要

随着民航业市场改革的推进,航空企业逐渐成为影响我国航空网络最为活跃的主体。海航航空是我国最大的股份制航空企业,其网络的空间结构和演化具有一定的典型性。因此,本文以海航航空为例,采用拓扑网络和复杂网络的相关指标,分析海航航空网络的空间结构及其演化特征。研究发现:海航航空网络仍处在不断的发展中,并逐渐呈现出小世界和无标度的特征;节点的中心性间具有较高的相关性,且介中心性位序-规模的变化速率要明显快于度中心性和邻近中心性;网络的中心性处于下降趋势,即网络内部节点的差异逐步减小;海航航空的枢纽选择从地方逐渐扩展到全国,并已基本形成了以北京、西安和海口为核心的网络结构,而其他层级结构尚不明显。

|

| [30] |

Social network analysis: A handbook [J].https://doi.org/10.1037/033461 URL [本文引用: 1] |

| [31] |

|

| [32] |

|

| [33] |

World Investment Report 2013 (Excerpts) Global Value Chains: Investment and Trade for Development [R/OL]. |

| [34] |

卢森堡经济模式对贵安新区发展的经验借鉴 [J].

正卢森堡是欧洲大陆惟一的大公国,国土面积仅为2590平方公里,人口只有53万,却是全球人均收入和生活水平最高的国家。根据国际货币基金组织(IMF)对2012年全球人均国内生产总值(GDP)的排名,卢森堡以10.75万美元位居世界第一位,比美国的人均GDP高出一倍多,是世界上人均最富裕的国家。作为国内市场狭小、资源相对贫乏的欧洲内陆国家,卢森堡如何实现国民

The experience of Luxembourg’s economic model for Gu'an New Area development.

正卢森堡是欧洲大陆惟一的大公国,国土面积仅为2590平方公里,人口只有53万,却是全球人均收入和生活水平最高的国家。根据国际货币基金组织(IMF)对2012年全球人均国内生产总值(GDP)的排名,卢森堡以10.75万美元位居世界第一位,比美国的人均GDP高出一倍多,是世界上人均最富裕的国家。作为国内市场狭小、资源相对贫乏的欧洲内陆国家,卢森堡如何实现国民

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}