童昕 , 王涛, 李沫

, 王涛, 李沫

北京大学城市与环境学院,北京 100871

Tong Xin, Wang Tao, Li Mo

中图分类号: F429.9;K902

文献标识码: A

文章编号: 1000-0069(2017)12-1823-08

收稿日期: 2017-02-12

修回日期: 2017-10-8

网络出版日期: 2017-12-20

版权声明: 2017 《地理科学》编辑部 本文是开放获取期刊文献,在以下情况下可以自由使用:学术研究、学术交流、科研教学等,但不允许用于商业目的.

基金资助:

作者简介:

作者简介:童昕(1975-),女,四川成都人,副教授,博士,主要从事工业地理与产业生态研究。E-mail:tongxin@urban.pku.edu.cn

展开

摘要

以无锡市为例,通过实地调研当地光伏产业链中多晶硅生产、电池元件生产、组件制造、相关设备生产、光伏设备运维服务,以及光伏用户等不同环节,从全球生产网络的视角,考察全球-本地联系在当地光伏产业链形成演化和技术发展动态中的具体表现。结论指出:① 无锡光伏产业在短短10 a之内从“两头在外”的发展模式到形成全产业链竞争优势,体现了新兴技术的全球生产网络技术加速更新和产业快速转移的新特点;② 本地相关产业集群通过技术引进、消化和改进为新技术突破规模化瓶颈,获取市场竞争力打下基础,并由此对全球光伏技术发展的路径产生了关键影响;③ 产业进一步发展需要针对能源转型的长期目标,着重探索能源消费侧的技术转型路径。

关键词:

Abstract

China’s photovoltaic (PV) industry has experienced rapid growth in recent years, gaining significant competitive advantage in the global market. This article investigated the global-local linkages in the photovoltaic industry in Wuxi, which facilitates the localization of imported technology to achieve economy of scale for production. Various firms along the value chain were interviewed, such as polysilicon producers, cell processers, module assemblers, production equipment suppliers, operation and maintenance service providers, as well as distributed PV users, to characterize the interactions between the global market and local actors. Conclusions point out that: 1) the development of Wuxi photovoltaic industry represents new form of technology transfer and industrial shift in emerging technology, in which the local learning in developing countries has a significant impact on the trajectory of the new technology. 2) The local industrial base enables the upscaling of production, which not only reduces the cost of photovoltaic technology dramatically, but also shapes the technological choice in world PV development. 3) While breaking through the bottleneck of production in the photovoltaic industry, Wuxi is now confronting the regime conflicts between distributed PV generation and traditional energy system. It calls for wider technological transition at the demands side.

Keywords:

全球太阳能光伏累计装机容量快速增长,从2000年不足0.3 GW[1],升至2015年的228 GW[2],15 a间光伏新增装机容量年平均增长率为49.5%[3]。其中,中国是目前全球最大,也是增长最快的光伏产品生产-消费国,2016年光伏产业总产值达3 360亿元,累计装机容量77.42 MW,为全球第一[4]。中国光伏产业超常规发展普遍被看作西方低碳能源市场拉动,与中国政府扶持下企业承接光伏技术转移,带来的后发追赶型模式的典型[5]。然而这种单向的技术转移视角并不能很好的解释中国在全球光伏产业发展中的异军突起[6]。

Hidalgo等人围绕产品异质性和技术联系的邻近性,尝试解释国家跨产业技术演化的动力机制[7,8]。实证分析进一步证实地区经济发展和结构转换的内生动力可以来自相关产业地理集中带来的本地学习能力,并进一步扩展到生产异质性产品的创新能力上,从而使国家和地区在新的产品领域形成比较优势[9]。因而地方专业化产业集群的升级方向和路径不能不考虑原有产业基础的技术联系[10]。中国在光伏产业形成系统化创新能力[11],深刻体现了这种技术演化路径的特点。本文以无锡光伏产业链发展为例,从全球产业网络的视角深入考察在这一新产品地方生产系统演化过程中,全球-本地的互动机制,试图揭示:① 产品的技术邻近性在微观企业联系中的具体表现;② 本地化的技术联系和市场联系在地方产业集群突破新产品规模经济瓶颈中的独特贡献;③ 消费侧的技术范式变革在能源转型长期战略中的关键意义。

针对空气污染、气候变暖和能源安全等问题,用低成本、清洁、可靠的能源替代化石能源成为全球能源结构转型的重要目标[12,13]。但是各国对于具体操作化目标和发展路线仍然存在广泛争议[14,15,16,17]。在多种可再生能源中,光伏太阳能发电在全球能源结构转型中扮演着越来越重要的角色,过去5 a年均增长率达到55%[18]。国际能源署预测到2050年光伏发电量将占到全球发电总量的16%[19,20]。不仅在发达国家新增光伏装机容量持续增长,诸如中国、印度等发展中国家也在大规模开展光伏发电系统的建设[21]。可再生能源发电技术的特点更适合分布式的电力生产消费模式,与现有的集中式电力生产供应模式存在技术范式的差异,因而能源转型是否能够实现系统化的技术范式突破对光伏产业未来发展有着深刻影响。

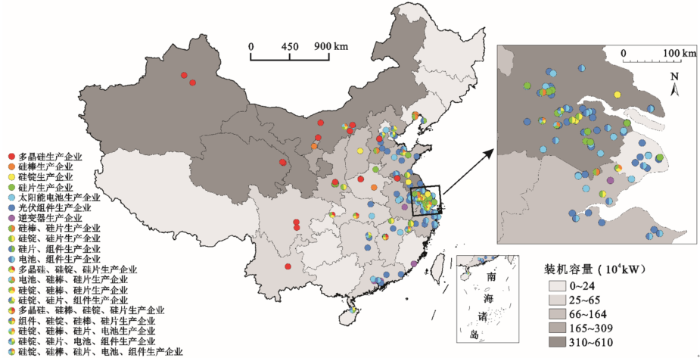

2010年以后,中国不仅在光伏组件生产上全面超越欧美和日本,并且将晶体硅锁定为市场主流技术[24]。中国的后来居上反映了光伏技术发展与传统产品生命周期的技术扩散方式存在差异,尽管欧美继续在专利上占据光伏技术研发的创新优势,但生产和应用环节对光伏技术的发展有着不可忽视的影响[25]。在光伏产业发展过程中,中国逐渐形成了差异化的地方产业集群,包括中西部地区以能源为导向的多晶硅生产基地、河北保定周边的硅片生产和加工基地、江苏苏南地区的太阳能电池和组件生产基地,以及广东等沿海省份的太阳能应用产品生产基地[26](图1)。其中,江苏是中国光伏产业最为集中的地区,2015年占全国光伏产业总产值的比重近2/3,仅无锡一市占比就超过10%[27]。

在突破规模经济瓶颈的过程中,外部市场提供的需求拉动尽管非常重要,但外部技术的植入与本地关键主体的学习和改进也同样不可或缺。早在2009年,英特尔创始人之一格罗夫就曾预言,中国有可能凭借电子产业的规模生产优势在光伏技术发展中超越欧美等技术研发的领先优势[28]。如今格罗夫预言成真,这个过程是如何发生的,值得深入检视。

本研究以无锡市(包括下辖的江阴市)为主要研究区域(图2)。无锡尚德曾经是引领国内光伏产业发展的龙头企业,并带动周边形成中国最大的光伏产业基地。截至2016年,无锡光伏产业共有规模以上企业37家,包括光伏材料、电池原件、光伏组件、逆变器、运维服务、数据管理等各生产环节。2011年无锡的太阳能电池产量占江苏产量的52%,占全国产量的28%,占全球产量的16%,外销率达到95%[29],形成了“世界光伏看中国,中国光伏看江苏,江苏光伏看无锡”的行业格局[30]。无锡

图1 中国光伏产业链的空间分布

资料来源:工业和信息化部 [

Fig.1 Distribution of photovoltaic industrial chain in China

周边是中国电力设备相关生产企业集中的地区,涌现出了一大批像尚德太阳能、江阴远景能源、上能电气等一批骨干和龙头企业,以无锡新能源产业园、风电科技产业园、江阴新能源科技产业园等产业基地为基础,形成了传统电力设备、风电、太阳能光伏并行发展的电力设备产业集群。

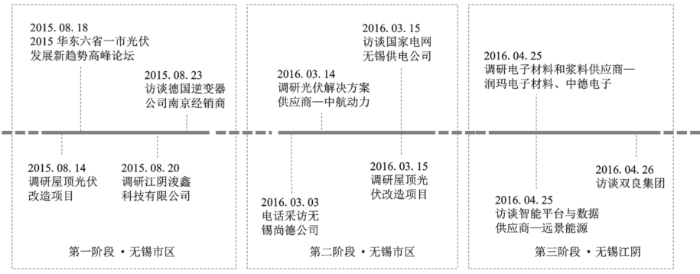

研究采用企业访谈的形式,访谈对象为光伏产业链各环节的代表性企业,包括光伏原料、晶硅生产、电池生产、组件制造、数据服务、光伏屋顶用户等。第一阶段的访谈主要集中在2015年8月,重点调研3家光伏屋顶用户和2家光伏组件企业和1家电池材料企业,其间还参加了华东六省一市光伏发展新趋势高峰论坛。2016年3月开展了第二阶段的调研,以无锡市区为主要调研区域,共访谈企业7家,包括组件制造、逆变器、数据服务、光伏系统运维企业和屋顶分布式光伏用户。第三阶段于2016年4月末在江阴集中访谈多晶硅还原炉制造商、浆料生产商等上游企业。访谈采用企业现场座谈形式,大多数内容有录音,并转录为文字记录。图3显示了调研过程。访谈采用半结构化问卷调查,内容包括企业光伏业务的发展过程、技术来源和市场联系,重点关注其全球联系与本地互动的具体形式。

研究采用全球生产网络分析方法考察光伏产业链中的全球-本地联系。首先根据访谈内容结合二手资料描绘出基于市场联系的无锡光伏产业地方生产网络结构。其次,重点阐述全球-地方联系在当地光伏产业的市场与技术变动中的具体表现,此处采用Bathelt等人提出的“全球通道-本地流传”的联系模式,按照产业链的组织特征,将不同环节的全球-地方联系串联在一起,呈现出整个地方生产网络中企业分散决策与集体学习的效果[31,32]。最后,围绕地方生产网络如何突破生产的规模经济瓶颈这一问题,结合调研访谈中的具体案例,阐述光伏产业各个环节如何借由全球-本地互动实现新兴产业的地方化集聚。

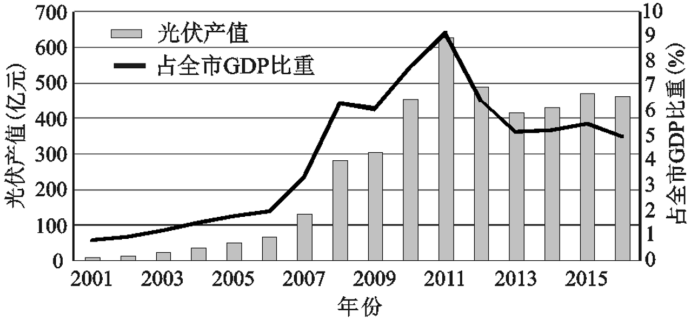

无锡光伏产业的发展可以分为4个阶段(图4)。① 起步阶段(2001~2005年)。 2001年施正荣博士带着光伏专利技术和产业经验从澳大利亚归来。在无锡市政府的组织协调下,当地6家国有企业出资共600万美元,组成了中澳合资的无锡尚德公司。 ② 发展阶段(2005~2011年)。2005年,随着全球可再生能源市场向好,尚德在海外迅速扩张。在尚德的影响下,无锡市出现了一大批光伏组件生产企业,包括浚鑫、海润、尚品等。 ③ 寒冬阶段(2011~2014年)。从2011年开始,由于欧盟的“双反”政策,海外市场对中国光伏产品征收平均高达47.6%的反倾销税。在光伏成本上升、产能过剩、价格下跌等市场环境的影响下,很多企业因此出现亏损甚至破产。 ④ 回暖阶段(2014年至今)。随着全球光伏市场快速增长,以及国内市场升温,无锡的光伏产业出现回暖。

图4 2001~2016年无锡光伏产值及占全市GDP比重(%)

Fig.4 Wuxi photovoltaic industry output and its proportion of GDP in 2001-2016 (%)

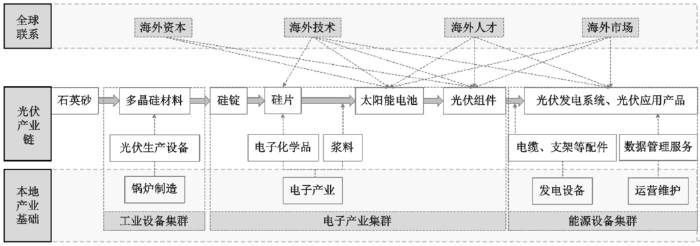

通过多年发展,无锡当地形成了以晶体硅电池为主的光伏产业链,包括从石英砂提炼出晶体硅材料,再生产出单晶硅棒或多晶硅锭,然后切片生产单晶硅片或多晶硅片,硅片通过覆盖银浆制成太阳能电池原件,再串联成组件,最后组装成光伏发电系统或产品。支持这一生产流程的材料和加工设备也多由当地提供,如多晶硅铸造炉、还原炉,光伏玻璃、铝浆、硅片切割液等,形成了较为完整的产业链。

无锡光伏产业链的各个环节都包含了全球-本地的紧密互动。图5揭示了海外资本、技术、人才、市场通过参与无锡光伏产业链从硅片制造到组件生产,再到光伏系统安装与技术支持,以及运行过程中提供数据服务的不同环节,与本地的工业设备集群、电子产业集群和能源设备集群之间展开的广泛互动。当地原有的专业化产业集群在这种全球-本地互动中发现新的市场机会,引进、学习并开发新技术,不断改进生产工艺,使得光伏产品实现规模化量产中遇到的瓶颈被快速突破。

弗农的产品生命周期理论认为,创新产品的形成、成熟和标准化在不同技术水平的国家里,发生的时间和过程不一样[33]。这一理论强调国家之间在创新产品中存在技术差距,保证新技术从发达国家到发展中国家的梯次转移。发达国家担任创新的角色,攫取高额的创新利润,再利用发展中国家的劳动力成本优势和市场扩大生产规模,并持续降低成本。

由于光伏产业在全球发展快速推进,上述技术转移的过程被大大压缩了。尽管欧美在光伏技术研发中拥有技术领先优势,但是在应用推广中面临两方面的困境。首先是生产环节难以实现规模化量产导致光伏产品价格居高不下。其次,由于可再生能源发电面临与传统电力生产之间的技术范式差别,光伏应用推广在发达国家也面临很大的困难。以德国为首的欧洲可再生能源政策希望通过特殊的电价机制为新技术打开市场。这一市场机遇通过企业家和技术人才的跨国流动与无锡当地的生产企业建立起市场和技术联系。

3.2.1 市场联系

全球市场需求通过跨国人才创业传递到本地,结合本地加工工业基础,从组件生产环节接入全球生产网络。无锡尚德就是一个典型。施正荣从澳洲回国创业,在缺少资金的情况下,很多地方当时都没有接受他的创业计划。但是无锡市政府出面协调组织本地几家国有企业参与了尚德最初的融资,使得尚德抓住了欧洲光伏市场补贴的机遇,利用国内生产的成本优势,赢得市场先机,并进一步借助海外资本市场筹措资金,实现了企业的快速成长。在海外上市过程中,无锡最初参与投资的国有资本从尚德退出。但在“尚德效应”的影响下,光伏产业投资一时成井喷之势,并且首先集中于组件生产,原料采购和产品市场都依靠海外。

图5 无锡光伏产业链中的全球-本地联系

Fig.5 Global-local linkage of photovoltaic industrial chain in Wuxi

组件生产规模扩大刺激了上游原材料价格飞涨,也带动了相关配套产业链的投资建设。这些产业投资与当地原有的专业化产业集群都有紧密的联系,包括工业设备产业集群、电子信息制造业集群、能源设备产业集群等。比如当地的民营企业双良集团,抓住光伏产业发展的机遇,利用自身在锅炉生产方面的技术积累,开拓多晶硅还原炉市场。电子信息制造企业发展与光伏生产相关的电子化学品。一般的金属加工制造企业也参与到平衡支架等配套产品的生产中来。在国内很多地区一哄而上发展光伏产业的背景下,无锡因为当地拥有多样化的制造业基础,在从光伏组件加工向全产业链延伸上更有优势。

不过,拥有上述制造基础优势的地区并不仅仅局限于无锡。欧美光伏市场的兴起在2005年以后带来全国光伏项目的热潮。同样具有出口加工生产基地优势的广东,以台商为龙头,也曾大力投入光伏产品的生产和研发。但经历欧美“双反”调查之后,国内光伏企业纷纷减产、倒闭,其中也包括曾经的光伏引领者无锡尚德。经过一波危机洗礼之后,江苏的光伏产业集中度更高了,这其中本地应用市场的支持发挥了非常重要的作用。2016年光伏累计装机容量,江苏省列全国第五,仅次于4个太阳能资源一类地区——新疆、甘肃、青海和内蒙古。其中,分布式光伏累计装机容量位列全国第二,仅次于浙江省[4]。作为太阳能资源三类地区的江苏,光伏应用水平超越了国内大多数光照条件更为优越的地区。

本地市场应用的推广,反过来又加强了光伏运维环节的全球联系。分布式能源的技术范式突破高度依赖运维环节的智能化电网管理。这一技术是在可再生能源发电技术应用过程中为了解决发电波动性的问题而逐步发展起来的。由于能源互联网技术的特点,分布式可再生能源运维环节的智能控制在地理上更加集中,可以通过互联网实现对遥远地区的风能、光伏等发电装置的远程监控、运行管理和维护。位于无锡江阴的远景能源,将其在风能发电管理的技术扩展到光伏云平台之上,成为国内光伏信息管理领域的后起之秀。

3.2.2 技术联系

无锡光伏产业通过快速学习,从制造环节向全产业链扩展。这一过程中,全球与本地的互动促进了技术的本地化。除了引进和学习,当地还出现了大量的本土技术创新。

在当地的产业网络中,尚德公司是产业技术网络的一个关键节点,不仅为当地光伏产业培养了大量的技术人才,也带动了周边配套企业的技术发展。尚德关于光伏技术最初的技术和知识来源是施正荣从海外带回来的。但随着尚德的建立,无锡当地逐渐发展起本地的光伏研发能力。即使在经历破产重组后,尚德研究院仍然自主研发了“冥王星”技术,刷新了晶硅电池的转换效率。在“尚德效应”的示范作用下,当时从新南威尔士大学回国创业的光伏博士就有12位之多,这些海外归国创业者成为全球与本地技术联系的关键纽带。

相关配套企业的自主研发进一步体现了本地技术学习和创新能力的重要性。在光伏生产的拉动下,海外为光伏配套的企业陆续到中国大陆投资建厂。一些关键材料的生产技术,如电子浆料,主要掌握在以杜邦、三星为首的跨国公司手中,以稳定的产品性能和高转换效率占据了绝大部分光伏银浆市场。无锡本地的半导体产业与晶体硅光伏生产技术有很高的技术相通性。为半导体企业配套的泓源光电和润玛电子,在发展光伏所需的银浆料、电子化学品等方面拥有良好的技术基础,因而能够开展技术研发,进入这一市场,并赢得一席之地。以润玛电子为例,企业原本为当地的半导体企业提供电子级化学品材料,光伏产业是其重点拓展的应用领域。企业在为客户提供电子化学品原料的同时,还针对单晶硅和多晶硅生产中的化学品污染问题,主动研发废化学品的回收再利用技术。为了提升自身在产业链竞争中的主动性,润玛电子还与国内高校和行业协会合作,参与制定光伏用电子化学品的国家标准

生产设备通常被看作发达国家对外技术转移过程中,知识编码化和内部化的重要途径[30]。无锡当地光伏设备生产中的技术进步则凸显了地方学习与创新能力的重要性。当地光伏制造设备的本地化率已经超过50%。这些企业并非仅仅模仿和引进国外技术,而是不断尝试改进提升。以双良集团为例,作为当地一家民营的锅炉生产企业,双良在德国西门子法多晶硅还原炉技术的基础上,自主研发全套生产设备,不断提升还原炉的生产效率。从最初德国技术每炉生产8对硅棒,不断升级,目前最新一代产品可实现每炉生产64对硅棒。除了提升生产效率,还通过炉体设计改进,将余热和废气重新导入还原炉循环利用,进一步节约了生产原料、能源消耗,以及污染治理的成本。

3.2.3 全球集聚的地方化效应

全球-本地之间的市场和技术联系促使光伏产业成功突破生产环节的规模经济瓶颈,并带来价格的快速下降。从全球来看,光伏技术呈现出新兴技术加速变化的特点,规模经济成为决定市场技术选择的关键。从2000年欧洲光伏市场启动,到2008年以后全球范围的加速扩张,光伏技术的更新换代延续了电子信息产业的技术进步驱动市场应用的特点。每个环节的规模化生产技术突破都可能带来整个产业链的市场动荡。

光伏技术发展中存在多个相互竞争的技术路线:单晶硅、多晶硅、非晶硅薄膜、碲化镉、铜铟镓硒等。随着终端市场需求的快速增长,这些竞争技术之间的优势与劣势不断发生变化,最终在市场选择中产生决定性作用的也是规模经济因素。晶体硅光伏技术因为与无锡本地已有的电子产业制造业基础具有更好的技术相通性,因而在突破生产环节的规模经济瓶颈方面占得先机,并进一步获得全球市场的主流地位。相比之下,薄膜技术尽管在实验开发阶段无论原料成本还是产品技术表现都曾一度拥有明显优势,但在规模化生产阶段却与现有的加工生产技术范式存在较大的差别,难以快速形成全产业链突破。

除了生产环节,市场应用是目前限制技术发展的另外一个关键环节。在海外市场遇阻,产业面临发展困境的情况下,国内应用市场的支持给当地光伏产业链提供了喘息的机会。并且,正是本地市场应用将光伏产业中的全球-本地联系从生产环节延伸到产品应用和运行维护环节。而可再生能源发电的智能控制呈现出更加显著的地理集中优势。应用平台的扩展不仅需要争取更多的用户,而且要和不同类型的可再生能源相互配合,在更大的区域范围内实现互联互补。

上述环环相套的发展过程体现了以光伏为代表的新兴产业,在全球生产网络的竞争环境下,所呈现出来的新的地理动态格局。首先,技术变动突破了从发达国家创新,到产品技术成熟后向发展中国家转移的传统模式,而是发展中国家利用自身规模化生产的优势,主动参与到前沿技术竞争之中;其次,规模经济突破本身构成创新技术发展的重要条件,特别是在技术走向多元化的新兴产业领域,能否快速实现规模化,往往成为技术能否成为市场主流的关键;最后,发展中国家自身的市场应用反过来也能影响全球技术发展的走势,技术创新和学习呈现出网络化和扁平化的特征。

无锡光伏产业链的发展对理解全球生产网络中的新兴技术推广具有重要意义。首先,无锡光伏产业在短短10 a间从两头在外的发展模式到形成全产业链竞争优势,体现了新兴技术加速更新和产业快速转移的新特点。在传统的全球生产网络中,起核心主导作用的往往是有自主品牌和研发生产能力的跨国公司。技术优势是跨国公司维系其在海外的竞争优势的重要前提。但光伏行业的发展折射出全球关于低碳能源转型的价值冲突。新兴技术面临与主流技术的范式之争。海外投资和技术不仅仅需要寻找低成本的生产区位,还需要避开主流技术范式的压制。地方对新技术的积极接纳,就成为沟通新兴市场和技术的重要保障。

在全球生产网络中,制造业的规模优势往往被看作比市场和研发优势低级的竞争力。然而,从无锡光伏产业链的发展中恰恰可以看到,突破规模生产的瓶颈在新兴技术的发展中起到了决定性的作用。这种规模经济的优势既嵌入在当地产业网络原有的技术系统之中,更在于针对市场需求的快速反应、积极学习和主动创新。

最后,单靠外部市场拉动和本地生产网络的响应,并不足以使光伏产业链真正扎根。在外部市场遭遇严冬的情况下,正是内需启动将产业链的技术优势从生产环节延伸到了运维服务环节,不仅帮助当地光伏硬件生产度过危机,而且在智能化的运维服务领域进入到全球创新合作的网络。这种优势是否能持续则取决于本地市场是否坚定认可低碳能源转型的大目标,并围绕需求侧的用户行为,推动分布式可再生能源发电的技术范式变革。

The authors have declared that no competing interests exist.

| [1] |

An innovation-focused roadmap for a sustainable global photovoltaic industry [J].https://doi.org/10.1016/j.enpol.2013.12.006 URL [本文引用: 1] 摘要

61We construct a two-factor learning curve model to quantify the effect of innovation.61We identify the industry-wide oversupply a barrier for incentivizing innovations.61We build a conceptual framework to inform an innovation-focused roadmap for the PV industry.61We recommend open data model for PV to accelerate policy and market innovations.

|

| [2] |

World Energy Outlook 2015[R] . |

| [3] |

Innovation and technology transfer through global value chains: Evidence from China's PV industry [J].https://doi.org/10.1016/j.enpol.2016.04.014 URL [本文引用: 1] 摘要

61The value chain analytical approach is synergized with the theories of technology transfer and innovation systems.61A detailed review of how China integrated itself into the global solar PV innovation system is provided.61Four main factors shape PV technology transfer to China across various value chain segments.61Innovation in cleaner energy technologies is a combination of global and national innovation processes.

|

| [4] |

国家能源局. 2016年光伏发电统计信息 [EB/OL]. .The statistics of photovoltaic power generation in The statistics of photovoltaic power generation in 2016 . |

| [5] |

Innovation and international technology transfer: The case of the Chinese photovoltaic industry [J].https://doi.org/10.1016/j.enpol.2010.10.050 URL [本文引用: 1] 摘要

China is the largest solar photovoltaic cell producer in the world, with more than one third of worldwide production in 2008, exporting more than 95 percent of what it produces. The purpose of this paper is to understand the drivers of this success and its limits, with a particular emphasis on the role of technology transfers and innovation. Our analysis combines a review of international patent data at a detailed technology level with field interviews of ten Chinese PV companies. We show that Chinese producers have acquired the technologies and skills necessary to produce PV products through two main channels: the purchasing of manufacturing equipment in a competitive international market and the recruitment of skilled executives from the Chinese diaspora who built pioneer PV firms. The success of these firms in their market is, however, not reflected in their performance in terms of innovation. Rather, patent data highlight a policy-driven effort to catch up in critical technological areas.Research Highlights?China has become the world leader in the production of PV cells and modules, but remains far behind industrialized countries in the more upstream segments of the photovoltaic industry. ?International technology transfers from industrialized countries to China have taken place through two main channels: the competitive market of manufacturing equipments, and labour mobility. ?Fierce competition between equipment manufacturers and public availability of core technology have prevented intellectual property rights from hindering technology transfers towards China. ?As compared with their foreign competitors, Chinese firms file many patents, but of low technical and commercial value. ?Chinese firms' innovation is focused on process rather than on products.

|

| [6] |

Spatial lifecycles of cleantech industries—The global development history of solar photovoltaics [J].https://doi.org/10.1016/j.enpol.2016.10.034 URL [本文引用: 1] 摘要

New industries develop in increasingly globalized networks, whose dynamics are not well understood by academia and policy making. Solar photovoltaics (PV) are a case in point for an industry that experienced several shifts in its spatial organization over a short period of time. A lively debate has recently emerged on whether the spatial dynamics in new cleantech sectors are in line with existing industry lifecycle models or whether globalization created new lifecycle patterns that are not fully explained in the literature. This paper addresses this question based on an extensive analysis of quantitative data in the solar PV sector. Comprehensive global databases containing 86,000 patents as well as manufacturing and sales records are used to analyze geographic shifts in the PV sector-檚 innovation, manufacturing and market deployment activities between 1990 and 2012. The analysis reveals spatial lifecycle patterns with lower-than-expected first mover advantages in manufacturing and market activities and an earlier entry of firms from emerging economies in manufacturing and knowledge creation. We discuss implications of these findings for the competitive positions of companies in developed and emerging economies, derive new stylized hypotheses for industry lifecycle theories, and sketch policy approaches that are reflexive of global interdependencies in emerging cleantech industries.

|

| [7] |

The product space conditions the development of nations .https://doi.org/10.1126/science.1144581 URL PMID: 17656717 [本文引用: 1] 摘要

Abstract: Economies grow by upgrading the type of products they produce and export. The technology, capital, institutions and skills needed to make such new products are more easily adapted from some products than others. We study the network of relatedness between products, or product space, finding that most upscale products are located in a densely connected core while lower income products occupy a less connected periphery. We show that countries tend to move to goods close to those they are currently specialized in, allowing nations located in more connected parts of the product space to upgrade their exports basket more quickly. Most countries can reach the core only if they jump over empirically infrequent distances in the product space. This may help explain why poor countries have trouble developing more competitive exports, failing to converge to the income levels of rich countries.

|

| [8] |

Country diversification, product ubiquity, and economic divergence .https://doi.org/10.2139/ssrn.1724722 URL [本文引用: 1] 摘要

Countries differ markedly in the diversification of their exports. Products differ in the number of countries that export them, which we define as their ubiquity. We document a new stylized fact in the global pattern of exports: there is a systematic relationship between the diversification of a country-檚 exports and the ubiquity of its products. We argue that this fact is not implied by current theories of international trade and show that it is not a trivial consequence of the heterogeneity in the level of diversification of countries or of the heterogeneity in the ubiquity of products. We account for this stylized fact by constructing a simple model that assumes that each product requires a potentially large number of non-tradable inputs, which we call capabilities, and that a country can only make the products for which it has all the requisite capabilities. Products differ in the number and specific nature of the capabilities they require, as countries differ in the number/nature of capabilities they have. Products that require more capabilities will be accessible to fewer countries (i.e., will be less ubiquitous), while countries that have more capabilities will have what is required to make more products (i.e., will be more diversified). Our model implies that the return to the accumulation of new capabilities increases exponentially with the number of capabilities already available in a country. Moreover, we find that the convexity of the increase in diversification associated with the accumulation of a new capability increases when either the total number of capabilities that exist in the world increases or the average complexity of products, defined as the number of capabilities products require, increases. This convexity defines what we term as a quiescence trap, or a trap of economic stasis: countries with few capabilities will have negligible or no return to the accumulation of more capabilities, while at the same time countries with many capabilities will experience large returns - in terms of increased diversification - to the accumulation of additional capabilities. We calibrate the model to three different sets of empirical data and show that the derived functional forms reproduce the empirically observed distributions of product ubiquity, the relationship between the diversification of countries and the average ubiquity of the products they export, and the distribution of the probability that two products are co-exported. This calibration suggests that the global economy is composed of a relatively large number of capabilities - between 23 and 80, depending on the level of disaggregation of the data - and that products require on average a relatively large fraction of these capabilities in order to be produced. The conclusion of this calibration is that the world exists in a regime where the quiescence trap is strong.

|

| [9] |

How do regions diversify over time? Industry relatedness and the development of new growth paths in regions .https://doi.org/10.1111/j.1944-8287.2011.01121.x URL [本文引用: 1] 摘要

abstract The question of how new regional growth paths emerge has been raised by many leading economic geographers. From an evolutionary perspective, there are strong reasons to believe that regions are most likely to branch into industries that are technologically related to the preexisting industries in the regions. Using a new indicator of technological relatedness between manufacturing industries, we analyzed the economic evolution of 70 Swedish regions from 1969 to 2002 with detailed plant-level data. Our analyses show that the long-term evolution of the economic landscape in Sweden is subject to strong path dependencies. Industries that were technologically related to the preexisting industries in a region had a higher probability of entering that region than did industries that were technologically unrelated to the region's preexisting industries. These industries had a higher probability of exiting that region. Moreover, the industrial profiles of Swedish regions showed a high degree of technological cohesion. Despite substantial structural change, this cohesion was persistent over time. Our methodology also proved useful when we focused on the economic evolution of one particular region. Our analysis indicates that the Link枚ping region increased its industrial cohesion over 30 years because of the entry of industries that were closely related to its regional portfolio and the exit of industries that were technologically peripheral. In summary, we found systematic evidence that the rise and fall of industries is strongly conditioned by industrial relatedness at the regional level.

|

| [10] |

中国对外贸易产品空间路径演化 [J].https://doi.org/10.11821/dlxb201606006 URL [本文引用: 1] 摘要

地区经济发展与其生产结构紧密相联。演化经济地理学认为,地区生产结构的演化受技术关联的影响,是一个路径依赖过程;一些研究也认为产业和区域政策等因素可能创造新路径,实现路径突破。本文沿用Hidalgo等定义的贸易产品空间方法,基于2001-2013年中国31个省区市的产品贸易数据,对中国出口产品空间(Product Space)的演化路径进行探讨。结果发现:中国四大区域—东部、中部、西部和东北地区的出口产品经历了较为明显的结构转型,不同区域的转型方向与路径各异。在2001-2007年间,四大区域的出口产品空间演化受到技术关联的显著影响,体现为路径依赖的过程。在2008-2013年间,东部、中部与东北地区的产品空间演化仍受技术关联的影响,而西部地区则更多受到产业和区域政策的推动,体现了路径突破的演化过程。本文研究启示,虽然中国区域生产结构演化一定程度上受制于现有区域能力、技术和知识积累,但是区域性制度政策创新可以突破原有路径,为区域发展创造新的机会。

Evolution of export product space in China: Path-dependent or path-breaking .https://doi.org/10.11821/dlxb201606006 URL [本文引用: 1] 摘要

地区经济发展与其生产结构紧密相联。演化经济地理学认为,地区生产结构的演化受技术关联的影响,是一个路径依赖过程;一些研究也认为产业和区域政策等因素可能创造新路径,实现路径突破。本文沿用Hidalgo等定义的贸易产品空间方法,基于2001-2013年中国31个省区市的产品贸易数据,对中国出口产品空间(Product Space)的演化路径进行探讨。结果发现:中国四大区域—东部、中部、西部和东北地区的出口产品经历了较为明显的结构转型,不同区域的转型方向与路径各异。在2001-2007年间,四大区域的出口产品空间演化受到技术关联的显著影响,体现为路径依赖的过程。在2008-2013年间,东部、中部与东北地区的产品空间演化仍受技术关联的影响,而西部地区则更多受到产业和区域政策的推动,体现了路径突破的演化过程。本文研究启示,虽然中国区域生产结构演化一定程度上受制于现有区域能力、技术和知识积累,但是区域性制度政策创新可以突破原有路径,为区域发展创造新的机会。

|

| [11] |

How China became a leader in solar PV: An innovation system analysis [J].https://doi.org/10.1016/j.rser.2016.06.061 URL [本文引用: 1] 摘要

In this paper we focus on understanding the rapid rise of the Chinese PV industry and its profound impact on the global PV industry. We investigate how it is possible that a nation that is still focusing on catching up in terms of industry, innovation and technology has been able to bring manufacturers from leading industrialized nations to their knees. This paper applies the framework of the Technological Innovation System (TIS), and also takes the context into account, in terms of the Chinese national innovation system (NIS) and the global PV TIS. It concludes that the rise of the Chinese PV TIS can be explained by the interaction of three context factors (the change in Chinese institutions, technology transfer, and the large European market) and specific PV TIS dynamics. The study empirically shows the importance of extending the national TIS studies by including the influences of context factors.

|

| [12] |

Providing all global energy with wind, water, and solar power, Part I: Technologies, energy resources, quantities and areas of infrastructure, and materials [J].https://doi.org/10.1016/j.enpol.2010.11.040 URL [本文引用: 1] 摘要

78 Replacing world energy with wind, water, and sun (WWS) reduces world power demand 30%. 78 WWS for world requires only 0.41% and 0.51% more world land for footprint and spacing, respectively. 78 Practical to provide 100% new energy with WWS by 2030 and replace existing energy by 2050.

|

| [13] |

Advanced technology paths to global climate stability: Energy for a greenhouse planet [J].https://doi.org/10.1126/science.1072357 URL PMID: 12411695 [本文引用: 1] 摘要

Stabilizing the carbon dioxide-induced component of climate change is an energy problem. Establishment of a course toward such stabilization will require the development within the coming decades of primary energy sources that do not emit carbon dioxide to the atmosphere, in addition to efforts to reduce end-use energy demand. Mid-century primary power requirements that are free of carbon dioxide emissions could be several times what we now derive from fossil fuels (approximately 10(13) watts), even with improvements in energy efficiency. Here we survey possible future energy sources, evaluated for their capability to supply massive amounts of carbon emission-free energy and for their potential for large-scale commercialization. Possible candidates for primary energy sources include terrestrial solar and wind energy, solar power satellites, biomass, nuclear fission, nuclear fusion, fission-fusion hybrids, and fossil fuels from which carbon has been sequestered. Non-primary power technologies that could contribute to climate stabilization include efficiency improvements, hydrogen production, storage and transport, superconducting global electric grids, and geoengineering. All of these approaches currently have severe deficiencies that limit their ability to stabilize global climate. We conclude that a broad range of intensive research and development is urgently needed to produce technological options that can allow both climate stabilization and economic development.

|

| [14] |

https://www .bp . |

| [15] |

London: PSI, 2013 . |

| [16] |

A path to sustainable energy by 2030 [J].https://doi.org/10.1038/scientificamerican1109-58 URL PMID: 19873905 [本文引用: 1] 摘要

Scientific American is the world's premier magazine of scientific discovery and technological innovation for the general public. Readers turn to it for a deep understanding of how science and technology can influence human affairs and illuminate the natural world.

|

| [17] |

Providing all global energy with wind, water, and solar power, Part II: Reliability, system and transmission costs, and policies [J].https://doi.org/10.1016/j.enpol.2010.11.045 URL [本文引用: 1] 摘要

78 We evaluate the feasibility of global energy supply from wind, water, and solar energy. 78 WWS energy can be supplied reliably and economically to all energy-use sectors. 78 The social cost of WWS energy generally is less than the cost of fossil-fuel energy. 78 Barriers to 100% WWS power worldwide are socio-political, not techno-economic.

|

| [18] |

global status report [R] . |

| [19] |

Technology roadmap: solar photovoltaic energy [R] . |

| [20] |

Medium-Term Renewable Energy Market Report 2014 [R] . |

| [21] |

Solar energy: Trends and enabling technologies [J].https://doi.org/10.1016/j.rser.2012.11.024 URL [本文引用: 1] 摘要

The global demand for energy is currently growing beyond the limits of installable generation capacity. To meet future energy demands efficiently, energy security and reliability must be improved and alternative energy sources must be investigated aggressively. An effective energy solution should be able to address long-term issues by utilizing alternative and renewable energy sources. Of the many available renewable sources of energy, solar energy is clearly a promising option as it is extensively available. Solar power, especially as it reaches more competitive levels with other energy sources in terms of cost, may serve to sustain the lives of millions of underprivileged people in developing countries. Furthermore, solar energy devices can benefit the environment and economy of developing countries. This paper illustrates the need for the utilization of alternative energy sources, evaluates the global scenario of installed generation systems, reviews technologies underlying various solar powered devices, and discusses several applications and challenges in this area. In addition, this paper addresses the costs of deployment, maintenance, and operation, as well as economic policies that promote installation of solar energy systems. (C) 2012 Elsevier Ltd. All rights reserved.

|

| [22] |

Industrial dynamism and the creation of a “virtuous cycle” between R&D, market growth and price reduction: The case of photovoltaic power generation (PV) development in Japan [J].https://doi.org/10.1016/S0166-4972(99)00146-7 URL |

| [23] |

Fast-Follower Industrial Dynamics: The Case of Taiwan’s Emergent Solar Photovoltaic Industry [J].https://doi.org/10.1080/13662716.2011.541104 URL 摘要

The world is on the cusp of major transformations of energy systems, with solar photovoltaic (PV) systems providing one of the most promising alternatives to fossil fuels. Amongst the countries moving to take advantage of the new production possibilities thus being opened up is Taiwan, employing in this new sector its characteristic strategies of fast followership that it has perfected in earlier industrial shifts involving semiconductors, ICT products and flat panel displays. This paper provides an interim assessment of Taiwan's early entry strategies, involving a focus on mainstream crystalline silicon solar cells, as well as entry into emerging niche sectors such as thin-film second-generation cells and concentrated solar cells utilizing novel semiconductor materials. Taiwan firms' fast-follower strategies are highlighted and assessed in light of the literature on industrial dynamics and catch-up processes generally. The paper makes a contribution to theory in building nine propositions regarding fast followership, based on prior industrial experiences and this latest episode in the solar PV industry. Taiwan's strategies as a model for China are discussed, while the paper proposes Taiwan as an alternative to the “closed” and “open” models of photovoltaic diffusion identified for Japan and the USA.

|

| [24] |

Interactions between renewable energy policy and renewable energy industrial policy: A critical analysis of China’s policy approach to renewable energies [J].https://doi.org/10.1016/j.enpol.2013.07.063 URL [本文引用: 1] 摘要

This paper analyzes China's policy approach to renewable energies and assesses how effectively China has met the ideal of appropriate interactions between renewable energy policy and renewable energy industrial policy. First we briefly discuss the interactions between these two policies. Then we outline China's key renewable energy and renewable industrial policies and find that China's government has well recognized the need for this policy interaction. After that, we study the achievements and problems in China's wind and solar PV sector during 2005-2012 and argue that China's policy approach to renewable energies has placed priority first on developing a renewable energy manufacturing industry and only second on renewable. energy itself, and it has not effectively met the ideal of appropriate interactions between renewable energy policy and renewable energy industrial policy. Lastly, we make an in-depth analysis of the three ideas underlying this policy approach, that is, the green development idea, the low-carbon leadership idea and indigenous innovation idea. We conclude that Chinas' policy approach to renewable energies needs to enhance the interactions between renewable energy policy and renewable energy industrial policy. The paper contributes to a deeper understanding of China's policy strategy toward renewable energies. (C) 2013 Elsevier Ltd. All rights reserved.

|

| [25] |

How the European Union’s and the United States’. anti-dumping duties affect Taiwan's PV industry: A policy simulation [J].https://doi.org/10.1016/j.rser.2015.08.036 URL [本文引用: 1] 摘要

To address continuous increases in global energy demand, countries around the world are developing coping plans that promote the development of renewable energy industries; a major focus of these nations' efforts is the photovoltaic (PV) industry. Since 2014, the European Union (EU) and the United States have imposed anti-dumping duties on PV industries in China and Taiwan. Because the development of the PV industry is affected by relevant government policies, Taiwan is ranked second in the world in PV production, and these duties will undoubtedly affect the future development of Taiwan's PV industry. Thus, PV manufacturers and the Taiwanese government are extremely concerned about the impact of the anti-dumping duties imposed on Taiwan's PV industry. In fact, the development structure of the PV industry is complex and dynamic. In this study, by assessing industry characteristics, the extant literature, and responses from interviews with experts, system dynamics (SD) is used to identify three key loops and explore the structure of the development of Taiwan's PV industry. Finally, trends in production capacity and financial conditions imposed by anti-dumping duties on Taiwan's PV industry are simulated to address the impact that different anti-dumping duty rates could produce. Repeated simulations are conducted to determine the critical rate at which this industry may disappear. In addition, relevant topics are discussed, and viable policy recommendations are proposed.

|

| [26] |

工业和信息化部. 《光伏制造行业规范条件》企业名单 [EB/OL]. [Ministry of Industry and Information Technology. The list of firms in compliance with “PV manufacturing industrial standards”. ]. Accessed 2017-11-17 |

| [27] |

刘纯. 光伏行业创新需求引爆新增长点 [EB/OL]. .The demands of PV industry innovation set off a new growth point . |

| [28] |

Grove Andy. How to Make an American Job Before It's Too Late [EB/OL]. Bloomberg, 2010. . |

| [29] |

新华网. 江苏太阳能电池产量占据全球四分之一 [EB/OL]. , 2010-06-09.. Jiangsu solar cell production accounts for a quarter of the world ..] Accessed 2017-05-20. |

| [30] |

-09-28 .-09-28 . |

| [31] |

Clusters and knowledge: local buzz, global pipelines and the process of knowledge creation [J].https://doi.org/10.1191/0309132504ph469oa URL [本文引用: 1] |

| [32] |

Regional development and the competitive dynamics of global production networks: An East Asian perspective [J].https://doi.org/10.1080/00343400902777059 URL [本文引用: 1] 摘要

Yeung H. W.-C. Regional development and the competitive dynamics of global production networks: an East Asian perspective, Regional Studies. The debate on the nature and dynamics of regional development in both academic and policy circles has now moved on from the earlier focus on endogenous regional assets to analysing the complex relationship between globalization and regional change. This position paper attempts to engage with this debate through the experience of regional development in East Asia. The p

|

| [33] |

International Investment And International Trade In The Product Cycle [J].https://doi.org/10.1002/tie.5060080409 URL [本文引用: 1] 摘要

This chapter describes international investment and international trade in the product cycle. It explains the United States market that offers certain unique kinds of opportunities. The United States market consists of consumers with an average income that is higher than that in any other national market, for instance, twice as high as that of Western Europe. The United States market is characterized by high unit labor costs and relatively unrationed capital compared with practically all other markets. This is a fact that conditions the demand for both consumer goods and industrial products. The Taiwanese and Japanese trade performances are perhaps the most telling ones in support of the projected pattern; both countries have managed to develop significant overseas markets for standardized manufactured products.

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}