姚晓明 , 朱晟君

, 朱晟君

北京大学城市与环境学院,北京 100871

Yao Xiaoming, Zhu Shengjun

中图分类号: F129.9

文献标识码: A

文章编号: 1000-0690(2019)02-0294-11

通讯作者:

收稿日期: 2018-01-14

修回日期: 2018-03-5

网络出版日期: 2019-02-20

版权声明: 2019 《地理科学》编辑部 本文是开放获取期刊文献,在以下情况下可以自由使用:学术研究、学术交流、科研教学等,但不允许用于商业目的.

基金资助:

作者简介:

作者简介:姚晓明(1986-),男,辽宁沈阳人,博士研究生,主要从事金融地理及产业动态演化研究。E-mail: yaoxm8042@163.com

展开

摘要

在梳理中国银行业改革历程和银行网点分布时空特征的基础上,提出银行空间扩张和地方性银行兴起是中国银行业空间演化的主要动力,并将该过程分解为银行操作距离和银行功能距离。在分析银行业空间演化过程的基础上,进一步引入地方银行业特征变量作为制约企业信贷获得的解释变量。实证结果表明,减小银行操作距离只能改善西部和东北地区企业信贷环境,而降低银行功能距离则能有效提高企业信贷获得,竞争型的地方银行市场能够提高非国有企业的信贷获得,银行本地化进程亦能提高非国有企业信贷获得。在转型经济的制度背景下,市场化力量能够有效扩大银行的安全信贷范围,而分权化过程有效地维护了地方信贷环境。

关键词:

Abstract

Under the background of China's transitional economy, the spatial organization structure of banks has been adjusted, and firm credit environment has changed accordingly. This article argues that spatial expansion of banks and rising of local banks are the main motive force for the spatial evolution of banking in China. We use operational distance and functional distance to describe the spatial evolution of banks. Based on the analysis of the spatial evolution of banking industry, this article introduces the local banking characteristics variables as the explanatory variables that restrict firm credit. The empirical results show that reducing the operational distance can only improve the corporate credit environment in the western and northeastern regions of China while reducing the functional distance can effectively improve firm credit. The competitive local banking market can enhance the credit access of non-state-owned enterprises. The localization of banks also increased the access of non-state-owned enterprises to credit, and so on. In the context of transitional economy, marketization forces can effectively increase the range of security credit, while the decentralization process has effectively improved the credit environment of enterprises.

Keywords:

1980年代以来世界范围内银行业发生巨大变化:职能分离[1]、空间重构[2,3]、层次明晰[4,5,6]等。与此同时,中国银行业实现了由专业化向市场化的转变,形成了由国有大型银行、股份制银行、城市商业银行、农村商业银行、邮政储蓄、外资银行等组成的商业银行体系[7]。而且银行业空间格局也发生了一系列演变[8,9,10]:国有银行基层网点调整[11,12]、股份制银行跨区域扩张[13]、城市商业银行和农村商业银行兴起[14]、外资银行大举进入[15,16,17]等等。银行组织体系和网点空间布局已悄然改变,呈现出鲜明的时代特征[12]。当前,银行仍是中国金融系统的主体,是企业重要的融资平台[18]。然而,由于企业与银行双方信息严重不对称,企业申请贷款时可能存在逆向选择问题、道德风险问题、代理人问题[19]。对此Pollard认为企业嵌入在具体的地方金融环境之中[20],“邻近”能够有效地化解上述问题[21,22],这也意味着银行业空间演化过程将重塑地方银行信贷市场。

鉴于此,Alessandrini等采用银行操作距离和银行功能距离来量化地方银行信贷市场的演变过程[23]。其中,银行操作距离是指借贷者与银行基层分支机构之间的距离,而银行功能距离则是指银行基层分支机构与上级决策中心之间的距离。一般来说,银行操作距离邻近有助于减小银行与企业之间信息交流成本[24],便于银行借助本地社会关系网络获取企业的“隐性”信息,准确判断企业违约风险。银行功能距离主要强调银行组织结构对信贷效率的影响[25],实际上银行基层网点直接接触申请借贷者,但多数信贷审批权掌握在上级行手中,银行组织结构的空间分离妨碍了有关借贷人信息在银行系统内部的传递效率。另外,基层网点作为信贷业务的代理者,在业绩提成制度的激励下与银行决策中心降低信贷风险的诉求相违背,二者利益并不完全一致。由于银行决策中心处于信息劣势,无法不加甄别地信任基层网点上传的信贷申请信息,这被称为代理人问题[23]。这样反而增大了银行决策中心贷款审核成本,谨慎放贷。由此可见,信息不对称问题和代理人问题制约着企业信贷获得。

然而,部分实证研究结果显示银行操作距离对企业信贷获得的影响存在争议:银行操作距离邻近也可能制约企业信贷获得或者不显著影响企业信贷[23,26,27]。Zhao等发现在英国银行操作距离减小并不会显著提高中小企业获得贷款的可能性[28]。事实上,由于地理邻近,银行反而掌握更多申请借贷企业信息,索要高额贷款利息[29,30],这被称为“赢者诅咒”现象(Winner’s Curse Phenomenon)[31]。此外,本地银行市场竞争者增多也会加剧中小企业信贷难度,面对激烈的信贷市场竞争,银行可能主动聚焦优质客户[32],回避“高风险”客户[33]。相比之下,银行功能距离对企业信贷获得影响的研究结论较为一致,现有研究普遍证明了它们之间显著的负相关关系[23,28],由于功能距离越大产生代理人问题的可能性越高,银行放贷更加慎重。不仅于此,地方信贷市场结构也制约着企业信贷获得[34]。

现有研究几乎全部以西方国家银行业为研究对象[19,23,28],实际上西方国家银行业空间演化主要是由于银行之间兼并重组造成的,这与中国银行业空间演化有着本质的不同。本文认为银行空间扩张和地方性银行兴起才是近年来中国银行业空间演化的真正动力。所以,有必要在中国转型经济的制度背景下重新审视银行业空间演化与企业信贷获得的关系,这具有理论和现实意义。综上,本文从中国银行业空间演化动态过程出发,拟回答以下2个问题:一是区域内银行机构的空间特征和动态演化过程如何影响企业信贷获得;二是在转型经济背景下,制度因素是否作用于银行业空间演化过程对企业信贷获得的影响。

本文中银行网点数量和空间分布数据整理自Wind数据库中的中国宏观数据和中国银监会(http://www.cbrc.gov.cn)的金融许可证信息数据(不含港澳台及海外地区银行网点登记信息)。为确保数据连贯,本文选用的数据涉及国有大型商业银行、政策性银行、股份制商业银行、城市商业银行、农村商业银行、邮政储蓄、外资银行共7种类型,一千余家银行。另外,文中银行分支机构是指除总行外的所有营业性分支,包括各级分行、支行、分理处、储蓄所以及各级分行的营业部等。

本文借鉴Alessandrini等采用的银行操作距离和银行功能距离的计量方法[23]:

1) 操作距离(Operational Distance)

式中,

2) 功能距离(Functional Distance)

式中,

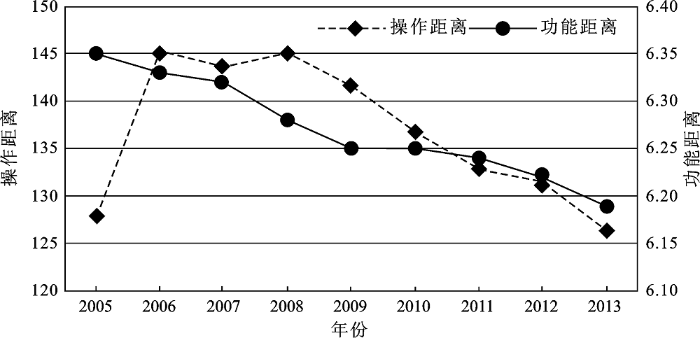

从2005年起,以国有大型商业银行相继启动上市计划为标志,中国银行业进入新一轮市场化改革时期。银行业演化过程表现出明显的时空特征。如图1所示,2005~2013年间全国平均的银行功能距离呈持续下降趋势。这说明随着地方性银行的兴起,减小了地方与银行决策中心之间的距离,缓解了地方信贷市场由于银行空间扩张而产生的代理人问题和信息不对称问题。换句话说,尽管银行跨区域经营可能造成规模不经济、内部信息传递效率低下,但在地方性银行发展较好的地区,反而抵消了因银行空间扩张而增大的功能距离,实际上有可能提高该地企业获得银行信贷的能力。

图1 2005~2013年中国平均操作距离和功能距离的变化趋势

Fig.1 China’s operational distance and functional distance during 2005-2013

与此同时,银行操作距离则表现出先升后降的演化特征,2008年达到最大值,随后持续降低。银行操作距离有如此波动的原因主要有两点:其一是2005年起国有大型银行上市后营利模式陆续转向追逐市场利润最大化,为此大批量撤并臃肿基层网点、调整空间布局,银行网点数量减少,造成银行操作距离增大;其二是随着银行业体制改革的不断深入,逐步取消了对非国有银行经营地域的限制,股份制银行和城市商业银行开始大规模异地设点经营,同时国有大型银行向发达地区新增大量网点,二者共同促进了地方银行网点密度的提高。

在空间上,银行操作距离和银行功能距离地区间差异十分明显。如图2所示,2008~2011年平均银行操作距离较小的地区分别是上海、北京、天津、江苏、浙江、山东、广东,均位于东部沿海地区,相比之下西藏、青海、新疆、内蒙古等西部省区的银行网点密度最低,而且东部地区的银行操作距离显著低于中西部地区。这说明地理邻近、减小操作距离仍是银行赢得市场竞争的必要手段。银行功能距离方面,拥有多家银行总行的北京银行功能距离最小,而且其他银行功能距离较小的省区也均是银行总行较为集中的地区,特别是城市商业银行数量较多的省份,如山东、辽宁等。这说明银行功能距离的大小主要与银行总行密集程度负相关,再次证明了地方性银行的建立能够有效减小本地的银行功能距离,降低信贷风险。

图2 2008~2011年中国各省市自治区平均操作距离和平均功能距离未包括港澳台数据

Fig.2 The average of operational distance and functional distance at the provincial level from 2008 to 2011

省级尺度上,银行操作距离和功能距离随时间的变化率表现出一定的空间特征。如图3所示,2006~2009年间银行操作距离只有在北京、天津、上海、黑龙江、福建、海南、云南、西藏8个省市区有所减小,其余地区均为上升阶段,西部地区(除云南、西藏外)尤为突出,说明西部地区银行网点大量撤并,银行操作距离明显增大。然而,接下来2010~2013年银行操作距离变化率则发生逆转,除吉林省外,其余地区操作距离均在减小。相比之下,东部地区和西部地区银行操作距离降低的幅度大于中部地区。这说明该阶段银行网点重点向金融市场发达地区布局,同时在地方政府的推动下地方性银行纷纷建立,银行网点密度有所增加。在银行功能距离方面,绝大部分地区的变化率与图1所示相似,呈下降趋势。其中只有北京、天津、上海、重庆、山西、吉林等地区的银行功能距离表现出阶段性增长,一方面可以认为上述地区金融市场对于区域外银行有巨大吸引力,另一方面说明上述地区本地银行发展滞后。此外,2006~2009年银行功能距离下降幅度较大的地区有江苏、浙江、河南、贵州,而到2010~2013年则主要集中在西北部,间接地呈现出了地方性银行建立的时空特点。

图3 全国各省市自治区操作距离和功能距离变化情况

Fig.3 Change of operational and functional distance in 2006-2013

本文研究银行业空间演化过程对企业信贷获得的影响,所以因变量为企业是否获得银行贷款。该值可以通过中国工业企业库中“利息支出”变量判断[35],其中利息支出大于零的企业说明其获得银行贷款,利息支出为零的企业则暂时没有银行贷款。由于这是二值选择问题,故本文采用Probit模型估计解释变量对企业获得银行信贷的作用[28]。

式中,

考虑到中国银行业的地方发展特征,本文还引入地方银行信贷市场结构和银行本地化程度作为解释变量,以衡量地方银行信贷市场的竞争程度和参与竞争的本地优势。

1) 赫芬达尔指数

本文用赫芬达尔指数(

式中,

2) 银行本地化程度

通过计算本地城市商业银行分支机构数量占本地所有银行分支机构总数的比重来衡量银行本地化程度(

事实上,有研究表明企业能否获得银行贷款受供给和需求两方面影响[37],由于本文解释变量已从银行供给角度引入,故有必要从企业需求角度选取控制变量。本文加入如下5个企业属性方面的控制变量:企业规模、企业年龄、企业所有制形式、企业是否出口、企业负债程度。企业数据全部来自中国工业企业数据库,本文借鉴前人的数据处理方法[38,39,40],删除部分缺失样本和一些有悖常理的样本。

具体的,企业规模(

本文假设企业所在区域的银行分布格局会影响企业能否获得贷款,具体的实证模型如下:

式中,

为避免内生性问题,本文因变量选取2013年企业数据,而银行操作距离、银行功能距离、地方银行业集中度、银行本地化程度则为2008~2011年的平均值。

首先对解释变量进行相关性检验,将相关性较强的解释变量拆分到不同的模型(相关系数大于0.6)。如模型(1~3)结果所示(表1),银行操作距离的系数显著为正,意味着企业与银行网点空间邻近不利于企业获得银行贷款,也就是说现阶段加大银行网点密度有可能造成企业信贷受限。由于操作距离邻近便于银行详尽掌握企业信息,银行转而成为强势一方,支配着贷款流向[30,42]。Zhao等也发现银行操作距离邻近反而增大了中小企业信贷受限的概率[28]。

表1 回归结果

Table 1 Regression results

| 企业是否获得银行贷款(Probit模型) | 企业利息支出占比(Tobit模型) | |||||

|---|---|---|---|---|---|---|

| 模型(1) | 模型(2) | 模型(3) | 模型(4) | 模型(5) | 模型(6) | |

| OD | 0.00119*** | 0.00127*** | 0.00131*** | 0.00004*** | 0.00004*** | 0.00004*** |

| FD | -0.0200*** | -0.0161*** | -0.000508* | -0.000263 | ||

| HHI | -0.823*** | -0.0896*** | ||||

| LOC | 2.372*** | 0.156*** | ||||

| size | 0.142*** | 0.143*** | 0.144*** | 0.00621*** | 0.00633*** | 0.00632*** |

| age | 0.00280*** | 0.00276*** | 0.00265*** | 0.00021*** | 0.00021*** | 0.00020*** |

| SOE | 0.261*** | 0.258*** | 0.254*** | 0.0197*** | 0.0194*** | 0.0189*** |

| CPOE | 0.563*** | 0.560*** | 0.552*** | 0.0241*** | 0.0238*** | 0.0232*** |

| FE | 0.0182 | 0.0128 | 0.00263 | -0.000843 | -0.00140 | -0.00207 |

| exp | 0.0936*** | 0.0926*** | 0.0918*** | 0.00463*** | 0.00447*** | 0.00455*** |

| ind | 0.0410*** | 0.0400*** | 0.0409*** | 0.00642*** | 0.00628*** | 0.00644*** |

| region | Included | Included | Included | Included | Included | Included |

| industry | Included | Included | Included | Included | Included | Included |

| 常数 | -0.253*** | -0.0256 | -0.464*** | -0.0571*** | -0.0313*** | -0.0659*** |

| N | 268821 | 268821 | 268821 | 268821 | 268821 | 268821 |

| log L | -132553.5 | -132542.8 | -132488.6 | 136127.1 | 136150.9 | 136177.6 |

| LR chi2 | 21465.7 | 21487.3 | 21595.5 | 5120.8 | 5168.3 | 5221.7 |

银行功能距离的系数显著为负,说明银行跨区域扩张过程导致进入地企业信贷受限。银行功能距离增大会产生银行分支机构与银行决策中心之间的信息不对称和代理人问题,妨碍了银行组织内部信息传递,降低了银行贷款决策效率。该发现与Alessandrini等[23]、Zhao等[28]的结论一致。进一步引入地方银行业集中度和银行本地化程度,结果显示地方银行业集中度的系数显著为负,也就是说区域内银行市场竞争有利于企业信贷获得。竞争型的银行信贷市场能够激发银行借贷意愿,尽可能地占据更多市场份额。另一方面,银行本地化程度的系数显著为正,说明基于地方网络的关系邻近有效地提高了企业获得贷款的可能性[43],证明了本地银行在盘活本地资金方面的重要作用。

控制变量方面,企业规模、企业年龄、出口企业的系数是显著为正的,符合预期。这说明客观的企业营利指标是银行贷款风险防控的重要参考依据,规模越大、成立时间越久、有产品出口的企业更容易被银行认为是信誉良好的企业。而企业所有制的结果显示,外资企业并不天然赢得银行青睐,相比之下国有企业和集体私营企业的回归结果则显著为正。此外,企业负债程度的系数也显著为正,说明在一定程度上企业负债率越高反而是企业经营状况良好的体现,已经取得银行信任的企业被视为信誉良好的企业,后来者的信贷分配存在模仿和跟随行为。除上述外,本文还以企业利息支出占收入比重作为被解释变量进行检验,由于该变量存在取值下限(最小值为0),故采用Tobit模型解决因变量取值受限问题。Tobit模型(4)~(6)的回归结果与前文基本一致,可以认为Probit模型的回归结果是稳健的。

接下来本文从区域差异的角度,进一步说明各地区的银行业演化过程对企业信贷的影响,结果如表2所示。其中,东部和中部地区银行操作距离和银行功能距离的回归结果与全国一致,而西部和东北地区则正好相反。银行操作距离方面,从图2可知西部省区的银行操作距离远远大于其他地区,说明西部地区银行网点数量不足是制约企业贷款获得的主要原因之一。另外,东北地区银行网点增长缓慢(图3),其中吉林甚至在2006~2013年间银行网点数量持续减少,可见新增银行网点数量不足也会造成企业信贷受限。这也就意味着提高西部和东北地区银行网点密度能有效地缓解企业信贷受限问题。银行功能距离方面,西部和东北地区吸引非本地银行进入可以帮助企业信贷获得,而且仅从银行本地化程度的回归系数的符号也证明了这一点。西部地区银行集中度和银行本地化程度的回归结果均不显著,原因在于西部地区本地银行发展滞后,尚未能弥补国有银行网点撤并留下的市场空缺。

表2 分四大经济区域的回归结果

Table 2 Regression results categorized by 4 economic plants

| 东部 | 中部 | 西部 | 东北 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| 模型(1) | 模型(2) | 模型(3) | 模型(4) | 模型(5) | 模型(6) | 模型(7) | 模型(8) | 模型(9) | |

| OD | 0.139*** | 0.151*** | 0.10*** | 0.09*** | -0.0004*** | -0.0005*** | -0.16*** | -0.084*** | |

| FD | -0.098*** | -1.254*** | 0.193*** | 10.33*** | |||||

| HHI | -23.04*** | 25.80*** | -0.237 | 124.1*** | |||||

| LOC | 33.24*** | 75.19*** | -2.039 | -93.50*** | |||||

| size | 0.144*** | 0.152*** | 0.135*** | 0.132*** | 0.059*** | 0.056*** | 0.151*** | 0.158*** | 0.151*** |

| age | 0.003*** | 0.003*** | 0.006*** | 0.006*** | -0.00162 | -0.00165 | -0.000591 | -0.00126 | -0.000591 |

| SOE | 0.229*** | 0.196*** | -0.0772 | 0.0578 | 0.139 | 0.136 | 0.122 | 0.179 | 0.122 |

| CPOE | 0.510*** | 0.426*** | 0.346*** | 0.474*** | 0.405*** | 0.390*** | 0.194** | 0.262*** | 0.194** |

| FE | -0.00409 | -0.068*** | -0.0782 | 0.0251 | 0.00939 | 0.00492 | 0.0328 | 0.106 | 0.0328 |

| exp | 0.138*** | 0.157*** | 0.0264 | 0.0168 | 0.0443 | 0.0563 | 0.255*** | 0.183*** | 0.255*** |

| ind | 0.090*** | 0.109*** | -0.00839 | 0.0126* | 0.070*** | 0.076*** | 0.070*** | 0.073*** | 0.070*** |

| industry | Included | Included | Included | Included | Included | Included | Included | Included | Included |

| 常数 | 5.897*** | -3.278*** | -1.869*** | -3.663*** | -0.217 | 1.104*** | -54.98*** | -35.50*** | 10.82*** |

| N | 173262 | 173262 | 51205 | 51205 | 25191 | 25191 | 19163 | 19163 | 19163 |

| log L | -90415.8 | -88576.4 | -16167.6 | -15509.5 | -6294.6 | -6325.6 | -10588.2 | -11362.7 | -10588.2 |

| LR chi2 | 20497.7 | 24176.6 | 3540.5 | 4856.6 | 291.0 | 228.9 | 3444.0 | 1895.1 | 3444.0 |

此外,地方银行业集中度的系数在东部地区显著为负,而中部和东北地区则显著为正。该结果表明,激烈的银行竞争有利于东部企业获得贷款,东部地区民营经济发达,竞争型的信贷市场促使银行主动扩大放贷范畴;然而中部和东北地区国有经济比重较大,垄断型的地区银行市场有利于这类地区企业信贷获得。类似的结论还可以从区分企业所有制类型的回归结果得到验证(表3),垄断的地方银行结构便于国有企业获得贷款,银行本地化程度越高反而阻碍国有企业获得贷款,东北地区银行本地化程度的系数显著为负也证明了这一点(表3)。除此之外,银行操作距离和银行功能距离对国有企业信贷获得的影响几乎完全不显著,主要原因在于国有企业与国有大型银行之间长期稳定的合作关系不受银行空间演化的影响。换句话说,中国银行业空间演化过程主要影响非国有企业信贷获得。

表3 区分企业所有制类型的回归结果

Table 3 Regression results categorized by firm ownership

| 国有企业 | 非国有企业 | |||||

|---|---|---|---|---|---|---|

| 模型(1) | 模型(2) | 模型(3) | 模型(4) | 模型(5) | 模型(6) | |

| OD | 0.000547* | 0.000506 | 0.000604* | 0.00128*** | 0.00138*** | 0.00143*** |

| FD | 0.0269 | 0.00231 | -0.0287*** | -0.0244*** | ||

| HHI | 5.775*** | -0.893*** | ||||

| LOC | -6.398*** | 2.968*** | ||||

| size | 0.212*** | 0.206*** | 0.210*** | 0.115*** | 0.116*** | 0.118*** |

| age | -0.00214* | -0.00216* | -0.00214* | 0.00407*** | 0.00402*** | 0.00387*** |

| exp | 0.376*** | 0.388*** | 0.379*** | -0.0719*** | -0.0733*** | -0.0742*** |

| ind | 0.239*** | 0.239*** | 0.239*** | 0.0487*** | 0.0475*** | 0.0482*** |

| region | Included | Included | Included | Included | Included | Included |

| industry | Included | Included | Included | Included | Included | Included |

| 常数 | -0.524*** | -2.118*** | -0.0936 | 0.474*** | 0.717*** | 0.173*** |

| N | 4975 | 4975 | 4975 | 263846 | 263846 | 263846 |

| log L | -2338.6 | -2326.1 | -2328.5 | -132154.7 | -132142.2 | -132060.0 |

| LR chi2 | 651.6 | 676.6 | 671.7 | 16934.5 | 16959.6 | 17124.0 |

改革开放以来,中国经济成功转型有赖于制度变迁,制度因素塑造了当下中国经济地理格局[44]。其中,市场化和分权化是中国经济转型的重要力量,市场力量的强化,增强了经济活动参与者的自主性,突出了市场配置资源的高效性;分权化则赋予地方政府更多的权力发展本地经济,导致了激烈的区域竞争,激励了地方政府参与竞争和地方保护行为的出现[45]。中国银行业改革是由国有银行市场化和地方性银行兴起二者合力推动的,因此本文分别将市场化力量(

回归结果(表4)印证了中国的制度转型的确影响到企业信贷获得。从表4的结果可见,市场化变量的系数显著为正,说明市场化程度深的地区能够促进企业获得贷款,充分满足企业融资需求,这点可以从浙江、江苏等地民营企业的经营状况得到佐证。银行操作距离本身系数为正,市场化与银行操作距离的交叉项系数亦为正,可见市场化强化了银行操作距离对企业信贷的影响,意味着市场化能够增大银行与企业间安全的信贷距离。另一方面,银行功能距离本身系数和交叉项系数均显著为负,说明市场化加重了银行空间扩张产生的代理人问题。一般来说,市场化程度深的地区银行业竞争激烈,视市场情形而定的银行基层网点放贷决策与银行决策中心可能存在较大分歧,降低了银行空间扩张的效率。

表4 含有交叉项的回归结果

Table 4 Regression results with intersection

| 模型(1) | 模型(2) | 模型(3) | |

|---|---|---|---|

| OD | 0.00119*** | -0.00120*** | 0.01325*** |

| FD | -0.0200*** | 0.627*** | -3.27*** |

| OD | 0.00271*** | ||

| FD | -0.674*** | ||

| OD | -0.0012*** | ||

| FD | 0.340*** | ||

| LIB | 3.913*** | ||

| DPT | -2.6123*** | ||

| size | 0.142*** | 0.143*** | 0.144*** |

| age | 0.00280*** | 0.00274*** | 0.00538*** |

| SOE | 0.261*** | 0.254*** | 0.138*** |

| CPOE | 0.563*** | 0.561*** | 0.371*** |

| FE | 0.0182 | 0.0161 | 0.0271 |

| exp | 0.0936*** | 0.0943*** | 0.2062*** |

| ind | 0.0410*** | 0.0408*** | 0.1085*** |

| region | Included | Included | Included |

| industry | Included | Included | Included |

| 常数 | -0.253*** | -4.004*** | 24.47*** |

| N | 268821 | 268806 | 265151 |

| log L | -132553.5 | -132450.7 | -124428.25 |

| LR chi2 | 21465.7 | 21661.2 | 35365.1 |

此外,分权化激发了地方力量的崛起,在中国经济转型中起到重要作用。从回归结果(表4)上看,分权化变量系数显著为负,意味着地方力量较强的地区不利于企业从银行获得贷款。事实上,地方力量的崛起往往萌生出地方保护主义,在银行领域表现为阻碍非本地银行进入,本地银行系统不成熟或者本地银行垄断市场都可能导致这类地区企业信贷受限。具体地,分权化变量与银行操作距离的交叉项系数为负,而与银行功能距离的交叉项系数则为正,表明分权化过程同时弱化了银行操作距离和银行功能距离对企业信贷获得的作用。这也印证了地方政府有意保护本地企业[46],帮助银行网点密集区域却仍信贷受限的企业获得贷款。另一方面,近年来地方政府有意培植起本地银行,减小了银行功能距离,减弱银行功能距离对企业信贷获得的负向影响,有效地改善了企业信贷环境。此外,本文引用

前人研究发现银行分支机构分布的空间差异会影响到企业信贷获得,在信息不对称的假设下,银行操作距离和银行功能距离的变化重新塑造了地方信贷市场。与西方国家银行业大规模兼并重组不同,中国银行业空间演化的动力主要来源于两方面:其一是银行的空间扩张,其二是地方性银行的兴起。因此在转型经济制度背景下的中国案例研究更具理论意义和现实意义。此外,现有研究缺乏动态的银行空间演化过程研究。

本文采用银行操作距离和银行功能距离随时间的变化来反映银行业空间演化过程,发现2005~2013年银行功能距离持续降低,而银行操作距离先升高再下降;东部沿海省市的银行操作距离显著小于中西部地区,而各地区银行功能距离除受地理距离影响外主要与银行总行数量负相关。另外,尽管大多数地区经历了银行网点数量先减少再增加过程,但是各省市区银行的动态演化速率差异较大,银行业市场化改革先重点撤并西部地区网点再加大东部地区银行网点密度。然而,地方性银行的建立打破了纯粹由市场利润决定银行网点密度的格局,使得西部地区银行操作距离同样大幅降低。同时,地方性银行建立的时序和数量决定了各地区银行功能距离的演化过程。

实证结果发现:整体而言,银行操作距离邻近不利于企业信贷获得,银行空间扩张过程产生的信息不对称和代理人问题在中国同样制约企业授信,竞争型的地方银行市场结构和地方性银行的建立能够有效地促进企业信贷获得。 现阶段银行是否放贷给企业仍建立在银企间良好关系的基础之上,然而通过增加银行网点减小操作距离的做法来改善企业信贷约束仅对西部和东北地区适用,而银行功能距离的降低的确可以帮助非国有企业信贷获得。 竞争型的地方银行市场能够提高非国有企业的信贷获得,相反垄断型的地方银行市场更有利于国有企业获得银行贷款。 虽然本地银行由于地理邻近便于形成稳固的银企关系,但这仅限于对非国有企业有效,银行本地化进程加剧了地方银行市场的竞争,提高了国有银行风险意识,弱化了国有企业的信贷能力。 在中国经济转型的制度背景下,市场化力量有效地缓解了企业与银行之间的信息不对等问题,提高了银行信贷的安全范围,但同时激烈的市场竞争也会增大银行异地扩张的经营风险;而分权化促进了地方力量的加强,地方政府一方面保护本地企业获得贷款,另一方面培植本地银行改善企业信贷环境。

在中国银行业改革的现实背景和中国转型经济的制度背景下,本文的研究结论对在省级尺度内协调银行与企业信贷关系具有重要的政策指导意义:首先,在适当的条件下继续大力度培植地方性银行建立、成长。本文注意到,地方性银行显著降低银行功能距离的负向作用,另外银行本地化程度越高能够显著提升非国有企业的贷款获得率。随着非国有经济在国民经济构成中的比重越发突出,融资问题长期困扰民营企业,着力发展本地的城市商业银行和农村商业银行有助于提高资本在本地循环速率,进而解决企业融资问题。但在国有经济仍占绝对主导地位的省区,地方性银行发展不宜过快。其次,银行空间扩张和网点调整在追求利润的同时还应充分考虑地方经济结构和银行信贷市场竞争环境。本文研究结论发现,在现阶段企业从银行得到贷款仍主要依靠银企关系的建立,意味着银行跨区域扩张存在一定的进入门槛。在银行层面,国有大型银行和股份制银行需加大国有经济占主导地位的地区银行网点密度,形成市场垄断对其信贷业务拓展更有帮助,尤其是在东北地区;城市商业银行未来应适当考虑向银行市场竞争显著促进企业信贷获得的地区扩张,显然进入东部或者西部地区利润空间更大。最后,地方政府应积极承担起银行和企业两端连接的桥梁作用,给予本地民营企业和新企业融资便利,继续发挥好分权化的地方力量在中国经济转型制度下的重要作用。

The authors have declared that no competing interests exist.

| [46] |

地方保护主义对地区产业结构的影响——理论与实证分析 [J].

本文旨在考察地区政府保护对地方产业结构的作用,对地区间产业结构趋同问题进行了研究。本文首先提出理论模型,在一个厂商投资行为模型中,从改变地区间贸易成本和政府直接投资两个方面引入地方政府行为变量,讨论政府行为对地区产业结构的影响。模型分析发现贸易成本的增加会促使地区间产业结构趋同,而政府直接投资对产业结构的影响并不确定,在一定情况下会促进地区间产业结构差异化。这些结论在随后进行的对中国近年地区和产业数据的实证研究中得到了验证。趋势分析发现样本年间我国地区产业结构差异的全国平均水平在逐年增大。而以地区为着眼点的计量回归分析则发现,在控制了运输条件、地区资源差异和产业结构等历史因素之后,政府变量对地区间产业结构差异变化有显著影响。政府设置贸易壁垒增加地区间贸易成本,会促进地区间产业结构趋同。政府的投资行为则在整体上促进了地区间产业结构的差异化。

Local protectionism and regional specialization: A model and econometric evidences .

本文旨在考察地区政府保护对地方产业结构的作用,对地区间产业结构趋同问题进行了研究。本文首先提出理论模型,在一个厂商投资行为模型中,从改变地区间贸易成本和政府直接投资两个方面引入地方政府行为变量,讨论政府行为对地区产业结构的影响。模型分析发现贸易成本的增加会促使地区间产业结构趋同,而政府直接投资对产业结构的影响并不确定,在一定情况下会促进地区间产业结构差异化。这些结论在随后进行的对中国近年地区和产业数据的实证研究中得到了验证。趋势分析发现样本年间我国地区产业结构差异的全国平均水平在逐年增大。而以地区为着眼点的计量回归分析则发现,在控制了运输条件、地区资源差异和产业结构等历史因素之后,政府变量对地区间产业结构差异变化有显著影响。政府设置贸易壁垒增加地区间贸易成本,会促进地区间产业结构趋同。政府的投资行为则在整体上促进了地区间产业结构的差异化。

|

| [1] |

|

| [2] |

Banking at the margins: a geography of financial exclusion in Los Angeles [J].https://doi.org/10.1068/a281209 URL [本文引用: 1] |

| [3] |

Chinese-American banking and community development in Los Angeles County [J].https://doi.org/10.1111/1467-8306.00316 URL [本文引用: 1] 摘要

Given the rapid increase of immigrant populations and ethnic communities in the U.S., it is surprising that so little attention has been paid to the role of ethnically owned banks in community development. Analyses of banking usually focus on developments such as mergers and consolidations within the mainstream financial sector. The academic literature on financial geography and the ethnic economy has established that the discriminatory and exclusionary practices of mainstream banks and other financial institutions play a significant role in impoverishing urban, low-income ghettos. Research on minority financial services largely focuses on the dynamics of informal financial establishments in ethnic neighborhoods. With the exception of research on African-American banks, there has been remarkably little scholarship on or even acknowledgement of ethnically owned formal financial institutions in minority communities. This article examines the parallel, co-respective growth of Chinese-American residents, businesses, and bank branches in Los Angeles, with special attention to spatial and temporal correlation. In particular, we explore the role of Chinese ethnic banks in altering commercial infrastructures and residential landscapes in Los Angeles County's Chinatown and the San Gabriel Valley ethnoburb area. This article is based on extensive quantitative data and on twenty-seven multilingual interviews conducted in 1999 with officers of Chinese-American banks.

|

| [4] |

新经济背景下金融空间系统演化 [J].https://doi.org/10.11820/dlkxjz.2009.06.019 URL Magsci [本文引用: 1] 摘要

<p>金融空间系统指一定区域范围内金融系统各种组成要素在空间中相互作用形成的空间结构,表现为金融机构和金融资本不同程度的空间集聚和分散。金融空间系统的变化通过三种渠道,经济效率、信用需求、信用获得影响地方发展。全球化、网络化、信息化背景下金融空间系统呈现出主流金融空间一体化,粘性金融地方竞争激烈,空间等级化特征显著,另类金融空间出现等发展趋势。金融空间系统演化的原始、微观动因来自金融机构和金融资本对不同空间潜在利润的追逐,同时深受全球化、国家金融制度变迁,信息技术进步、金融危机爆发等外生宏观因素的影响。</p>

Study on financial spatial system evolution under new economic background .https://doi.org/10.11820/dlkxjz.2009.06.019 URL Magsci [本文引用: 1] 摘要

<p>金融空间系统指一定区域范围内金融系统各种组成要素在空间中相互作用形成的空间结构,表现为金融机构和金融资本不同程度的空间集聚和分散。金融空间系统的变化通过三种渠道,经济效率、信用需求、信用获得影响地方发展。全球化、网络化、信息化背景下金融空间系统呈现出主流金融空间一体化,粘性金融地方竞争激烈,空间等级化特征显著,另类金融空间出现等发展趋势。金融空间系统演化的原始、微观动因来自金融机构和金融资本对不同空间潜在利润的追逐,同时深受全球化、国家金融制度变迁,信息技术进步、金融危机爆发等外生宏观因素的影响。</p>

|

| [5] |

Centralization and marginalization: The Chinese banking industry in reform [J].https://doi.org/10.1016/j.apgeog.2011.09.003 URL [本文引用: 1] 摘要

Based on the distribution patterns of the sub-branches and saving outlets of the Industrial and Commercial Bank of China and the Bank of China in prefectural cities in China between 2001 and 2009, this paper examines how these two Chinese state-owned commercial banks may centralize their operations and thus lead to the possible marginalization of the provision of basic banking services to low value-added customers. The restructuring of SOCBs may not result in high levels of layoff due to the state objectives of minimizing both operational costs and political risks. When the politically sensitive issue of (un)employment is not taken into account, the more economically developed cities with larger populations and the more developed telecommunication facilities experience a higher level of centralization of their banking operations. The centralization of banking operations in China is, however, not always at the expense of savings outlets, despite the merging of savings outlets with sub-branches in various Chinese cities. There is circumstantial evidence to suggest the convergence thesis is not applicable to the banking industry in China, which is different from the conventional argument in financial geography that the centralization and marginalization of banking operations are two sides of the same coin as in the restructuring of the Anglo-American banking industries. This difference could be due to the hybrid ownership structures of state-owned commercial banks in China where the boundaries between public and private property rights are blurred.

|

| [6] |

北京金融服务业空间格局及模式研究 [J].

利用北京行政区域界限基础地理底图及相关统计年鉴,通过GIS技术及INTERNET查询、调研等途径,将北京行政区内银行、保险、证券及其他金融服务业网点机构进行矢量化。借助区位熵、均匀度指数和空间缓冲区分析,测度北京金融服务业空间分布特征,结果显示:①北京市金融服务业,特别是保险和证券服务业主要集中在中心区和郊区内沿,空间上呈现出以金融街、中央商务区所在的中心区为核心,其他区县(政府所在地)为外围的"核心-外围"结构;②中心区内金融服务业空间布局相对均匀,三环和四环之间金融机构分布较多,与国外大都市服务业的"单中心集聚,总体扩散"区位特征基本相同;③不同类型金融机构空间布局差异较大,各金融机构总部集中在金融街布局,中国人民银行集中布局在金融街-前门广场东西路上,呈线状布局,证券在北二环和北四环之间相对集中,保险服务业相对分散。④以金融街为中心作缓冲区多边形,间隔距离为2km,做10个缓冲区,发现在0—2km内服务网点机构密度最大,6—8km和8—10km内机构数量最多。⑤金融服务业空间布局模式多样化。

Study on the spatial pattern and structure of financial service industry in Beijing .

利用北京行政区域界限基础地理底图及相关统计年鉴,通过GIS技术及INTERNET查询、调研等途径,将北京行政区内银行、保险、证券及其他金融服务业网点机构进行矢量化。借助区位熵、均匀度指数和空间缓冲区分析,测度北京金融服务业空间分布特征,结果显示:①北京市金融服务业,特别是保险和证券服务业主要集中在中心区和郊区内沿,空间上呈现出以金融街、中央商务区所在的中心区为核心,其他区县(政府所在地)为外围的"核心-外围"结构;②中心区内金融服务业空间布局相对均匀,三环和四环之间金融机构分布较多,与国外大都市服务业的"单中心集聚,总体扩散"区位特征基本相同;③不同类型金融机构空间布局差异较大,各金融机构总部集中在金融街布局,中国人民银行集中布局在金融街-前门广场东西路上,呈线状布局,证券在北二环和北四环之间相对集中,保险服务业相对分散。④以金融街为中心作缓冲区多边形,间隔距离为2km,做10个缓冲区,发现在0—2km内服务网点机构密度最大,6—8km和8—10km内机构数量最多。⑤金融服务业空间布局模式多样化。

|

| [7] |

|

| [8] |

我国商业银行规模经济问题与金融改革策略透析 [J].

本文通过对中国商业银行 1 994— 2 0 0 0年的经营情况的实证分析 ,估算出了各大银行的成本 -规模弹性。在此基础上 ,本文指出 :商业银行经营过程中长期存在的不良贷款沉淀以及放款上的所有制偏好等问题已成为现阶段影响我国金融机构成本 -规模弹性的重要因素 ,而隐藏于它们背后的产权制度安排上的缺陷、金融领域的长期垄断 ,以及民营银行的“国民待遇”等问题则应成为下一步改革的关键

On the economies of scale in the state-owned banks and strategy analysis of financial reform .

本文通过对中国商业银行 1 994— 2 0 0 0年的经营情况的实证分析 ,估算出了各大银行的成本 -规模弹性。在此基础上 ,本文指出 :商业银行经营过程中长期存在的不良贷款沉淀以及放款上的所有制偏好等问题已成为现阶段影响我国金融机构成本 -规模弹性的重要因素 ,而隐藏于它们背后的产权制度安排上的缺陷、金融领域的长期垄断 ,以及民营银行的“国民待遇”等问题则应成为下一步改革的关键

|

| [9] |

西方金融地理学研究进展及其启示 [J].https://doi.org/10.3969/j.issn.1007-6301.2005.04.003 URL Magsci [本文引用: 1] 摘要

<p>金融地理学作为一门新兴的分支学科,已受到越来越多地理学者的重视。本文试图总结国外学者在金融地理学领域的研究进展,阐述其当前主要研究议题,提出对我国金融地理研究的启示。国外金融地理学的研究主要经历了以下几个发展阶段:自20世纪70年代以来,地理学家开始关注金融机构在引导特定地区资本流动过程中所起的作用; 80年代,学者们转向研究金融在西方社会中的角色、特定金融制度的空间组织与运作、金融中心的发展、金融流动与产业发展的关系等; 90年代以来,金融地理研究中出现了三个贯穿、且相互增强的研究对象,即解除管制、技术创新及全球化,相关研究中出现了文化制度转向。当前主要研究议题包括: 金融中心的形成、发展及萎缩; 金融排除及其带来的地方货币系统的研究;货币地理学研究等。根据国外的研究进展及经验,我国可以在金融服务网络的空间格局、货币流地域差异、金融排除及其相关的社会问题等方面展开研究。</p>

Progress in financial geography in western countries and its implications for Chinese geographers .https://doi.org/10.3969/j.issn.1007-6301.2005.04.003 URL Magsci [本文引用: 1] 摘要

<p>金融地理学作为一门新兴的分支学科,已受到越来越多地理学者的重视。本文试图总结国外学者在金融地理学领域的研究进展,阐述其当前主要研究议题,提出对我国金融地理研究的启示。国外金融地理学的研究主要经历了以下几个发展阶段:自20世纪70年代以来,地理学家开始关注金融机构在引导特定地区资本流动过程中所起的作用; 80年代,学者们转向研究金融在西方社会中的角色、特定金融制度的空间组织与运作、金融中心的发展、金融流动与产业发展的关系等; 90年代以来,金融地理研究中出现了三个贯穿、且相互增强的研究对象,即解除管制、技术创新及全球化,相关研究中出现了文化制度转向。当前主要研究议题包括: 金融中心的形成、发展及萎缩; 金融排除及其带来的地方货币系统的研究;货币地理学研究等。根据国外的研究进展及经验,我国可以在金融服务网络的空间格局、货币流地域差异、金融排除及其相关的社会问题等方面展开研究。</p>

|

| [10] |

中国地区银行业金融系统的区域差异 [J].https://doi.org/10.3321/j.issn:0375-5444.2007.12.001 URL [本文引用: 1] 摘要

随着中国国金融服务业不断深人改革以及对外资金融机构的逐渐开放.金融服务业的空间格局更为复杂。以银行业为例.区域内服务地域范围不同的银行金融机构的组合已经引起人们的重视.这种组合就构成了地区金融系统(地区银行系统)。地区金融系统内的银行金融机构可以划分为包括国有商业银行、政策性银行、全国性股份制商业银行、外资银行等的外来型银行金融机构.以及包括城市商业银行(城市信用社)、农村信用社(农村合作银行)等的本地型银行金融机构。研究表明:地区金融系统存在着萌芽期、发展期以及成熟期三个发展阶段.不同阶段具有明显的特点。地区金融系统受到地区经济发展水平、产业结构、地方政策以及地区金融素养等因素影响。采用定性和定量相结合的方法.利用中国30个省市(自治区)的数据.分析了中国各地区金融系统的区域差异。在各地区金融系统中,外来型银行金融机构表现为:国有银行的分支机构处于相对主导的地位;外资银行集中于重要结点;全国性股份制商业银行区域性集中趋势明显:对于本地型银行金融机构则具有城市商业银行分布不均:农村信用社填充国有银行撤出地区空白,但实际发挥的作用有限等特点。

Regional differences of local banking systems in China .https://doi.org/10.3321/j.issn:0375-5444.2007.12.001 URL [本文引用: 1] 摘要

随着中国国金融服务业不断深人改革以及对外资金融机构的逐渐开放.金融服务业的空间格局更为复杂。以银行业为例.区域内服务地域范围不同的银行金融机构的组合已经引起人们的重视.这种组合就构成了地区金融系统(地区银行系统)。地区金融系统内的银行金融机构可以划分为包括国有商业银行、政策性银行、全国性股份制商业银行、外资银行等的外来型银行金融机构.以及包括城市商业银行(城市信用社)、农村信用社(农村合作银行)等的本地型银行金融机构。研究表明:地区金融系统存在着萌芽期、发展期以及成熟期三个发展阶段.不同阶段具有明显的特点。地区金融系统受到地区经济发展水平、产业结构、地方政策以及地区金融素养等因素影响。采用定性和定量相结合的方法.利用中国30个省市(自治区)的数据.分析了中国各地区金融系统的区域差异。在各地区金融系统中,外来型银行金融机构表现为:国有银行的分支机构处于相对主导的地位;外资银行集中于重要结点;全国性股份制商业银行区域性集中趋势明显:对于本地型银行金融机构则具有城市商业银行分布不均:农村信用社填充国有银行撤出地区空白,但实际发挥的作用有限等特点。

|

| [11] |

转型时期快速增长城市国有银行区位变化研究 [M]Research on the location change of urban state owned banks in rapid growth during the transition period .// |

| [12] |

银行业改革与国有商业银行网点空间布局——以中国工商银行和中国银行为例 [J].https://doi.org/10.11821/yj2013010012 [本文引用: 2] 摘要

伴随着国有商业银行股份制改革,中国国有商业银行在全国的网点布局发生了战略性变化。在经营效益的驱动下,银行采取集中化策略,大幅度减少基础网点数目,而增加支行数目。两类网点地理分布的空间不均衡性加大,地理集中度上升。网点布局向主要经济增长极集中,而从边疆地区与落后地区撤离。对中国工商银行和中国银行基础网点及支行空间分布统计分析表明,两者的两类网点的地理分布在股份制改革后均发生了较大的变化,基础网点更加接近主要客户群体,支行则更加集中在经济发展较好的地区。结合自身的业务优势与特点,两者在两类网点的区位选择上也有一定的差别。国有商业银行经营效益导向的网点布局战略将可能带来落后地区的金融排斥问题。

Banking reform and locational strategy of state-owned commercial banks in China: An empirical study of Industrial and Commercial Bank of China and Bank of China .https://doi.org/10.11821/yj2013010012 [本文引用: 2] 摘要

伴随着国有商业银行股份制改革,中国国有商业银行在全国的网点布局发生了战略性变化。在经营效益的驱动下,银行采取集中化策略,大幅度减少基础网点数目,而增加支行数目。两类网点地理分布的空间不均衡性加大,地理集中度上升。网点布局向主要经济增长极集中,而从边疆地区与落后地区撤离。对中国工商银行和中国银行基础网点及支行空间分布统计分析表明,两者的两类网点的地理分布在股份制改革后均发生了较大的变化,基础网点更加接近主要客户群体,支行则更加集中在经济发展较好的地区。结合自身的业务优势与特点,两者在两类网点的区位选择上也有一定的差别。国有商业银行经营效益导向的网点布局战略将可能带来落后地区的金融排斥问题。

|

| [13] |

中国全国性股份制商业银行地理分布特征研究 [J].https://doi.org/10.3969/j.issn.1000-8462.2014.02.004 URL [本文引用: 1] 摘要

分析了中国12家股份制商业银行网点在省域、市域层次的分布格局,运用集中度指数、基尼系数、Moran指数揭示我国股份制商业银行的集群特征。研究发现:①股份制商业银行网点主要聚集在东部沿海发达城市,呈由东向西递减的格局。②股份制商业银行在省份/地区存在发展阶段差异性,形成了不同的分布结构类型。③股份制商业银行具有空间聚集性,空间相关性为正相关。④股份制商业银行的空间发展为多因素作用,包括我国银行准人政策、银行企业盈利驱动和城市社会经济条件等。

The geographic distribution characteristics research of Chinese joint-stock commercial bank .https://doi.org/10.3969/j.issn.1000-8462.2014.02.004 URL [本文引用: 1] 摘要

分析了中国12家股份制商业银行网点在省域、市域层次的分布格局,运用集中度指数、基尼系数、Moran指数揭示我国股份制商业银行的集群特征。研究发现:①股份制商业银行网点主要聚集在东部沿海发达城市,呈由东向西递减的格局。②股份制商业银行在省份/地区存在发展阶段差异性,形成了不同的分布结构类型。③股份制商业银行具有空间聚集性,空间相关性为正相关。④股份制商业银行的空间发展为多因素作用,包括我国银行准人政策、银行企业盈利驱动和城市社会经济条件等。

|

| [14] |

新世纪中国银行体制改革与地方银行机构网点的空间分布——兼与全国性商业银行的比较 [J].

20世纪90年代以来,中国银行体制改革催生了以城市商业银行和农村商业银行为代表的地方银行,它们以中小企业和城乡居民为主要服务对象,弥补了全国性商业银行的市场空缺,在我国金融体系中发挥着日益重要的作用。对银行体制改革的分析发现,城市商业银行和农村商业银行从仅限于单一地区经营,到放开地域经营限制,允许跨区域设立分行后,两银行机构网点的数量呈现出快速增长趋势,其网点的地理分布在改革前后发生了较大变化。将两银行与全国性商业银行的网点分布进行对比发现,其总行布局与地方经济发展刺激下的金融需求有着更为密切的联系;两银行跨区域设立异地分行的区位选择具有较大差别:城市商业银行优先选择发达地区,而后采取全国性战略布局和区域性梯度式布局两种模式扩张;农村商业银行则优先考虑欠发达地区,然后主要以区域内跳跃式扩张。

Banking reform and location strategy of local banks in the new century: In comparison with national banks .

20世纪90年代以来,中国银行体制改革催生了以城市商业银行和农村商业银行为代表的地方银行,它们以中小企业和城乡居民为主要服务对象,弥补了全国性商业银行的市场空缺,在我国金融体系中发挥着日益重要的作用。对银行体制改革的分析发现,城市商业银行和农村商业银行从仅限于单一地区经营,到放开地域经营限制,允许跨区域设立分行后,两银行机构网点的数量呈现出快速增长趋势,其网点的地理分布在改革前后发生了较大变化。将两银行与全国性商业银行的网点分布进行对比发现,其总行布局与地方经济发展刺激下的金融需求有着更为密切的联系;两银行跨区域设立异地分行的区位选择具有较大差别:城市商业银行优先选择发达地区,而后采取全国性战略布局和区域性梯度式布局两种模式扩张;农村商业银行则优先考虑欠发达地区,然后主要以区域内跳跃式扩张。

|

| [15] |

跨国银行在华发展区位研究 [J].https://doi.org/10.3969/j.issn.1004-9479.2001.04.004 URL [本文引用: 1] 摘要

自中国对外开放以来 ,跨国银行积极在华开拓业务 ,目前已有来自 18个国家和地区的6 8家银行在中国设立了 15 8家分行。本文阐述了在华跨国银行的发展规律及区位指向 ,并初步分析了跨国银行来华发展的区位行为和动机 ,展望跨国银行在中国发展的策略取向

Study on the location of multinational banks in China .https://doi.org/10.3969/j.issn.1004-9479.2001.04.004 URL [本文引用: 1] 摘要

自中国对外开放以来 ,跨国银行积极在华开拓业务 ,目前已有来自 18个国家和地区的6 8家银行在中国设立了 15 8家分行。本文阐述了在华跨国银行的发展规律及区位指向 ,并初步分析了跨国银行来华发展的区位行为和动机 ,展望跨国银行在中国发展的策略取向

|

| [16] |

外资银行在中国的区位选择 [J].https://doi.org/10.3321/j.issn:0375-5444.2009.06.007 URL [本文引用: 1] 摘要

金融业渐进式准入制度直接影响外资银行进入中国市场。伴随改革开放进程,外资银行最初聚集于经济特区和北京,进而扩散到上海、天津、大连和广州,以致于中西部城市,如重庆、成都和西安。外资银行的分行支行尤为聚集于珠三角、长三角和京津等经济发达地区,代表处则偏好聚集于北京和上海。条件逻辑模型统计结果表明,外资银行所有权优势、内部化优势和中国城市的区位优势,尤其是制度优势和银行业规模经济优势共同影响外资银行分支机构在中国的区位选择。外资银行尤为偏好金融规模效应显著、对外资银行准入管制较少的贸易型城市,央行总部及其区域性分行所在城市也是外资银行偏好的区位。由于代表处与分行或支行的功能差异,两者的区位行为存在一定不同。

An empirical study on the locational choices of foreign banks in China .https://doi.org/10.3321/j.issn:0375-5444.2009.06.007 URL [本文引用: 1] 摘要

金融业渐进式准入制度直接影响外资银行进入中国市场。伴随改革开放进程,外资银行最初聚集于经济特区和北京,进而扩散到上海、天津、大连和广州,以致于中西部城市,如重庆、成都和西安。外资银行的分行支行尤为聚集于珠三角、长三角和京津等经济发达地区,代表处则偏好聚集于北京和上海。条件逻辑模型统计结果表明,外资银行所有权优势、内部化优势和中国城市的区位优势,尤其是制度优势和银行业规模经济优势共同影响外资银行分支机构在中国的区位选择。外资银行尤为偏好金融规模效应显著、对外资银行准入管制较少的贸易型城市,央行总部及其区域性分行所在城市也是外资银行偏好的区位。由于代表处与分行或支行的功能差异,两者的区位行为存在一定不同。

|

| [17] |

The locational distribution of foreign banks in China: A disaggregated analysis [J].https://doi.org/10.1080/00343401003614282 URL [本文引用: 1] 摘要

He C. and Yeung G. The locational distribution of foreign banks in China: a disaggregated analysis, Regional Studies. This paper examines the location choices made by foreign banks of different organizational form and size in China. Results from the conditional logit models suggest smaller foreign banks tend to pursue the ‘follow-the-customer’ strategy, while larger banks are likely to use the ‘follow-the-competitor’ strategy in China. The agglomeration effect is more important than the first-mover cities as a determinant of the location choices make by foreign banks in China. This finding could be partially explained by the location-bounded institutional variables that are unable to be fully reconciled with the recent deregulation policies. He C. et Yeung G. La distribution géographique des banques étrangères en Chine: une analyse désagrégée, Regional Studies. La présente étude cherche à analyser le choix d'emplacement des banques étrangères en Chine en fonction de leur structure organisationnelle et de leur taille différentes. Les résultats provenant des modèles logit conditionnels laissent supposer qu'en Chine les plus petites banques étrangères ont tendance à poursuivre la stratégie de ‘suivre le client’, alors que les plus grandes banques sont plus susceptibles d'adopter la stratégie de ‘suivre le concurrent’. L'effet d'agglomération s'avère plus important que ne l'est le phénomène du premier arrivé dans les grandes villes comme déterminant des choix d'emplacement des banques étrangères en Chine. Ce résultat pourrait, du moins en partie, s'expliquer par des variables institutionnelles qui sont délimitées géographiquement et qui ne peuvent pas être conciliées avec les politiques récentes de déréglementation. Banques étrangères69Choix d'emplacement69Modèle logit conditionnel69Chine He C. und Yeung G. Verteilung der Standorte ausl01ndischer Banken in China: eine disaggregierte Analyse, Regional Studies. In diesem Beitrag werden die Standortentscheidungen ausl01ndischer Banken verschiedener Organisationsformen und Gr0208en in China untersucht. Aus den Ergebnissen konditionaler Logit-Modelle geht hervor, dass kleinere ausl01ndische Banken in China meist eine Strategie des 67Dem-Kunden-Folgens“ w01hlen, w01hrend gr0208ere Banken meist auf eine Strategie des 67Der-Konkurrenz-Folgens“ setzen. Der Agglomerationseffekt spielt als Determinant für die Standortentscheidungen ausl01ndischer Banken in China eine gr0208ere Rolle als die Pionierst01dte. Dieses Ergebnis l01sst sich teilweise durch die standortgebundenen institutionellen Variablen erkl01ren, die sich nicht vollst01ndig mit den aktuellen Deregulationspolitiken in Einklang bringen lassen. Ausl01ndische Banken69Standortentscheidungen69Konditionales Logit-Modell69China He C. y Yeung G. La distribución de ubicación de los bancos extranjeros en China: un análisis desglosado, Regional Studies. En este artículo analizamos las decisiones de ubicación tomadas por bancos extranjeros de diferentes formas de organización y tama09os en China. Los resultados de los modelos logit condicionales indican que en China los bancos extranjeros más peque09os tienden a optar por la estrategia de ‘seguir al cliente’ mientras que los bancos más grandes tienden a usar la estrategia de ‘seguir a la competencia’. El efecto de aglomeración desempe09a un papel más importante que el de las ciudades pioneras para determinar las decisiones de ubicación que realizan los bancos extranjeros en China. Estos resultados podrían explicarse en parte por las variables institucionales vinculadas a la ubicación que no pueden reconciliarse totalmente con las recientes políticas de desregulación. Bancos extranjeros69Decisiones de ubicación69Modelo logit condicional69China

|

| [18] |

转型时期中国金融体系中的地方治理与银行改革的互动研究 [J].[本文引用: 1] 摘要

本文立足于中国渐进式的转轨路径,分析了转型期地方治理与银行改革的互动表现和影响。计划轨和市场轨的相互制约与影响,在地方治理与银行改革方面,突出地表现为地方政府在自身改革的不同阶段,从自身利益出发,利用银行改革中的制度缺陷,不断改变对银行金融资源的争夺方式,由初始的直接行政干预到对银行决策施加影响,再过渡到目前通过逃废银行债务等间接争夺银行资源,而中央政府和银行体系则通过不断完善自身的管理体制和健全风险管理机制来抵御地方政府的争夺。双方博弈的结果在相当长的时期内都对全社会金融资源的配置、货币政策的有效传导和金融微观主体的经营产生了深远的影响。本文建议从地方政府职能转换、投融资体制改革,以及深化金融体制改革、完善银行治理结构等方面入手,逐步形成地方治理和银行改革的良性互动。

The interaction between local governance and banking reform in China's financial system during the transitional period .[本文引用: 1] 摘要

本文立足于中国渐进式的转轨路径,分析了转型期地方治理与银行改革的互动表现和影响。计划轨和市场轨的相互制约与影响,在地方治理与银行改革方面,突出地表现为地方政府在自身改革的不同阶段,从自身利益出发,利用银行改革中的制度缺陷,不断改变对银行金融资源的争夺方式,由初始的直接行政干预到对银行决策施加影响,再过渡到目前通过逃废银行债务等间接争夺银行资源,而中央政府和银行体系则通过不断完善自身的管理体制和健全风险管理机制来抵御地方政府的争夺。双方博弈的结果在相当长的时期内都对全社会金融资源的配置、货币政策的有效传导和金融微观主体的经营产生了深远的影响。本文建议从地方政府职能转换、投融资体制改革,以及深化金融体制改革、完善银行治理结构等方面入手,逐步形成地方治理和银行改革的良性互动。

|

| [19] |

Innovation, SMEs and the liability of distance: the demand and supply of bank funding in UK peripheral regions [J].https://doi.org/10.1093/jeg/lbw011 URL [本文引用: 2] 摘要

This paper considers geographical variations in the demand and supply of bank finance for innovative firms in the UK. It uses a detailed survey on the finances of almost 40,000 UK Small and Medium Sized Enterprises for 2011 – 2013 to investigate both the extent and type of applications for bank finance by innovative firms in peripheral regions, whether funders accept their applications and whether acceptance rates reflect objective criteria, such as credit scores, or their location. The paper finds evidence of higher demand for bank finance for innovative firms in peripheral areas, but that these firms are more likely to be discouraged from applying. However, there is strong evidence that innovative firms in peripheral regions are more likely to have their applications for finance rejected, even when controlling for factors such as credit score. The findings suggest that geography matters in the financing of innovative firms and firms in peripheral areas may suffer a “liability of distance” which potentially reinforces regional disparities. The implications of these findings for public policy are outlined.

|

| [20] |

Small firm finance and economic geography [J].https://doi.org/10.1093/jeg/lbg015 URL [本文引用: 1] 摘要

This paper argues that firm finance is something of a 'black-box' in economic geography, a largely take-for-granted aspect of production. Focusing on small firms, the paper argues that firm finance warrants analysis, not simply to 'add' to knowledge and to form another sub-discipline of economic geography, but in order to further develop and refine our understanding of uneven development. The paper explores the neglect of firm finance in economic geography and highlights some of the contributions of literatures in eco-nomics and business. Finally, the paper outlines three points of intersection between these disparate, usually disciplinary-bound, literatures in business, economics, and economic geography: the place-bound nature of firms, the social character of economic relations, and third, the power relations and asymmetries inherent in financial relationships. These intersections are used to critique existing small firm finance literatures and to outline the contours of an emerging research agenda in economic geography. Copyright 2003, Oxford University Press.

|

| [21] |

A 'possibilist' approach to local financial systems and regional development: the Italian experience. In Martin R L(ed.). Money and Space Economy . |

| [22] |

Decentralized versus centralized financial systems: is there a case for local capital markets? [J].https://doi.org/10.1093/jeg/lbh071 URL [本文引用: 1] |

| [23] |

Banks, distances and firms' financing constraints [J].

Bank deregulation and progress in information technology altered the geographical diffusion of banking structures and instruments, and reduced operational distance between banks and local economies. Although, the consolidation of the banking industry promoted the geographical concentration of banking decision-making centres and increased functional distance between local banking systems and local borrowers. This paper focuses on the impact that these spatial diffusion-concentration phenomena had on the financing constraints of Italian firms over the period 1996--2003. Our findings show that greater functional distance stiffened financing constraints, especially for small firms, while smaller operational distance did not always enhance credit availability. Copyright 2009, Oxford University Press.

|

| [24] |

|

| [25] |

Small business credit availability and relationship lending: The importance of bank organizational structure [J].https://doi.org/10.1111/1468-0297.00682 URL [本文引用: 1] 摘要

Abstract This paper models the inner workings of relationship lending, the implications for bank organisational structure, and the effects of shocks to the economic environment on the availability of relationship credit to small businesses. Relationship lending depends on the accumulation over time by the loan officer of `soft' information. Because the loan officer is the repository of this soft information, agency problems are created throughout the organisation that may best be resolved by structuring the bank as a small, closely-held organisation with few managerial layers. The shocks analysed include technological innovations, regulatory regime shifts, banking industry consolidation, and monetary policy shocks.

|

| [26] |

Informed finance and technological change: Evidence from credit relationships [J].https://doi.org/10.1016/j.jfineco.2005.12.001 URL [本文引用: 1] 摘要

This paper empirically investigates the effect of “informed finance” on technological change. The theoretical literature offers conflicting predictions on whether the information of financiers fosters or inhibits firms’ innovation. Using data from a sample of Italian manufacturing firms, we find that the information of firms’ main banks, proxied by the duration of credit relationships, promotes innovation. This positive effect is economically and statistically more significant for product than for process innovations. Nonetheless, the role of relationship banks in innovation is quite unsophisticated: they do not foster internal research but rather fund the relevant investments that the introduction and acquisition of new technologies entails.

|

| [27] |

Banks and innovation: Microeconometric evidence on Italian firms [J].https://doi.org/10.1016/j.jfineco.2008.01.001 URL [本文引用: 1] 摘要

In this paper we investigate the effect of local banking development on firms innovative activities, using a rich data set on innovation for a large number of Italian firms over the 1990s. There is evidence that banking development affects the probability of process innovation, particularly for firms in high-tech sectors, in sectors more dependent upon external finance, and for firms that are small. The evidence for product innovation is much weaker and not robust. There is also some evidence that banking development reduces the cash flow sensitivity of fixed investment spending, particularly for small firms, and that it increases the probability they will engage in R&D.

|

| [28] |

SMEs, banks and the spatial differentiation of access to finance [J].https://doi.org/10.1093/jeg/lbw029 URL [本文引用: 6] 摘要

By utilizing the SME Finance Monitor and a unique dataset on the geographical location of all bank branches in 11 UK economic regions, this paper examines the relevance of spatial differentiation on SMEs’ access to bank finance during the period of economic weakness following the 2007 financial crisis. We find evidence suggesting the presence of a regional-specific effect on SMEs’ access to bank finance. Our findings show that greater functional distance between bank headquarters and branches exacerbates the credit constraints faced by local SMEs although the impact of a smaller operational distance between branches and local SMEs is inconclusive, ceteris paribus. Our finding holds over a battery of robustness tests.

|

| [29] |

Does distance still matter? The information revolution in small business lending [J].https://doi.org/10.1111/1540-6261.00505 URL [本文引用: 1] 摘要

Abstract The distance between small firms and their lenders is increasing, and they are communicating in more impersonal ways. After documenting these systematic changes, we demonstrate they do not arise from small firms locating differently, consolidation in the banking industry, or biases in the sample. Instead, improvements in lender productivity appear to explain our findings. We also find distant firms no longer have to be the highest quality credits, indicating they have greater access to credit. The evidence indicates there has been substantial development of the financial sector, even in areas such as small business lending.

|

| [30] |

Distance, lending relationships, and competition [J].https://doi.org/10.1111/j.1540-6261.2005.00729.x URL [本文引用: 2] 摘要

We study the effect on loan conditions of geographical distance between firms, the lending bank, and all other banks in the vicinity. For our study, we employ detailed contract information from more than 15,000 bank loans to small firms comprising the entire loan portfolio of a large Belgian bank. We report the first comprehensive evidence on the occurrence of spatial price discrimination in bank lending. Loan rates decrease with the distance between the firm and the lending bank and increase with the distance between the firm and competing banks. Transportation costs cause the spatial price discrimination we observe.

|

| [31] |

Moneylenders and bankers: price-increasing subsidies in a monopolistically competitive market [J].https://doi.org/10.1016/S0304-3878(96)00443-9 URL [本文引用: 1] 摘要

In many areas of the world, a significant part of the cost of obtaining a good or service is the cost of enforcing the contracts entailed in its provision. We present models of markets with endogenous enforcement costs, motivated by studies of rural credit markets. We show that subsidies may have perverse effects under monopolistic competition, increasing prices or inducing exit. Higher prices (interest rates) result from the loss of scale economies or from negative externalities among suppliers. The models are consistent with the puzzling evidence that infusions of government-subsidized formal credit have not improved the terms offered by moneylenders.

|

| [32] |

Information technology and financial services competition [J].https://doi.org/10.2139/ssrn.296179 URL [本文引用: 1] 摘要

We analyze how two dimensions of technological progress affect competition in financial services. While better technology may result in improved information processing, it might also lead to low-cost or even free access to information through, for example, informational spillovers. In the context of credit screening, we show that better access to information decreases interest rates and the returns from screening. However, an improved ability to process information increases interest rates and bank profits. Hence predictions regarding financial claims' pricing hinge on the overall effect ascribed to technological progress. Our results generalize to other financial markets where informational asymmetries drive profitability, such as insurance and securities markets. Copyright 2003, Oxford University Press.

|

| [33] |

A lender-based theory of collateral [J].https://doi.org/10.1016/j.jfineco.2006.06.002 URL [本文引用: 1] 摘要

We consider an imperfectly competitive loan market in which a local relationship lender has an information advantage vis--vis distant transaction lenders. Competitive pressure from the transaction lenders prevents the local lender from extracting the full surplus from projects. As a result, the local lender inefficiently rejects marginally profitable projects. Collateral mitigates the inefficiency by increasing the local lender's payoff from precisely those marginally profitable projects that she inefficiently rejects. The model predicts that, controlling for observable borrower risk, collateralized loans are more likely to default ex post, which is consistent with the empirical evidence. The model also predicts that borrowers for whom local lenders have a relatively smaller information advantage face higher collateral requirements, and that technological innovations that narrow the information advantage of local lenders, such as small business credit scoring, lead to a greater use of collateral in lending relationships.

|

| [34] |

The effect of credit market competition on lending relationships [J].https://doi.org/10.2307/2118445 URL [本文引用: 1] 摘要

This paper provides a simple framework showing that the extent of competition in credit markets is important in determining the value of lending relationships. Creditors are more likely to finance credit-constrained firms when credit markets are concentrated because it is easier for these creditors to internalize the benefits of assisting the firms. The paper offers evidence from small business data in support of this hypothesis.

|

| [35] |

Exports, productivity, and credit constraints: A firm-level empirical investigation of China [J].https://doi.org/10.2139/ssrn.1461399 URL [本文引用: 1] 摘要

Recent Melitz-type (2003) intra-industry heterogonous trade models argue that a firm's productivity has significant effects on the firm's exports. This paper examines how a firm's credit constraints as well as its productivity affect its export decisions. We imbed the firm's credit constraints into a Melitz-type general-equilibrium model by endogenizing the probability of the success of firm-specific projects. We show that,all else equal,it is easier for firms to enter the export market if (1) the probability of the success of their project is higher and consequently they have easier access to external finance from financial intermediaries; or (2) they are foreign invested firms and have lower credit constraints. We test these theoretical hypotheses using firm-level data from Chinese manufacturing industries and find strong evidence supporting the predictions of the model.

|

| [36] |

The benefits of lending relationships: Evidence from small business data [J].https://doi.org/10.2307/2329133 URL [本文引用: 1] 摘要

This paper empirically examines how ties between a firm and its creditors affect the availability and cost of funds to the firm. We analyze data collected in a survey of small firms by the Small Business Administration. The primary benefit of building close ties with an institutional creditor is that the availability of financing increases. We find smaller effects on the price of credit. Attempts to widen the circle of relationships by borrowing from multiple lenders increases the price and reduces the availability of credit. In sum, relationships are valuable and appear to operate more through quantities rather than prices.

|

| [37] |

银行信贷配给与中小企业贷款——一个内生化抵押品和企业规模的理论模型 [J].

本文在吸收其他文献合理成分的基础上 ,通过考虑贷款抵押品的信号甄别机制和银行审查成本对贷款额的影响 ,将借款企业的资产规模、风险类型与抵押品价值相联系 ,构建了内生化抵押品和企业规模的均衡信贷配给模型。根据该模型 ,在信贷配给中被剔除的主要是资产规模小于银行所要求的临界抵押品价值的中小企业和部分高风险企业。本文的理论模型对于更好地理解市场经济及转型经济条件下的中小企业融资难问题提供了启示。

On the bank credit rationing and loan of small and medium-sized enterprises (SMEs) .

本文在吸收其他文献合理成分的基础上 ,通过考虑贷款抵押品的信号甄别机制和银行审查成本对贷款额的影响 ,将借款企业的资产规模、风险类型与抵押品价值相联系 ,构建了内生化抵押品和企业规模的均衡信贷配给模型。根据该模型 ,在信贷配给中被剔除的主要是资产规模小于银行所要求的临界抵押品价值的中小企业和部分高风险企业。本文的理论模型对于更好地理解市场经济及转型经济条件下的中小企业融资难问题提供了启示。

|

| [38] |

中国工业生产率的增长与收敛 [J].

本文采用的数据包括1998年和2005年中国所有规模以上工业企业。我们主要探讨了三个问题。第一,中国工业经济的增长多大程度上是由生产率的改变所驱动的;第二,不同所有制类型的企业生产率表现有何差异,包括对国有企业和各种非国有企业的比较;第三,我们探讨了沿海、东北部、中部和西部等四个主要经济区域的生产率水平是否存在收敛的问题。我们发现企业进入和退出样本对生产率增长有着特殊的影响。在1998年至2005年间,这种进入和退出促进了中国工业生产率的增长,并且加快了内陆省份生产率对沿海地区的追赶。

Productivity growth and convergence across China’s industrial economy .

本文采用的数据包括1998年和2005年中国所有规模以上工业企业。我们主要探讨了三个问题。第一,中国工业经济的增长多大程度上是由生产率的改变所驱动的;第二,不同所有制类型的企业生产率表现有何差异,包括对国有企业和各种非国有企业的比较;第三,我们探讨了沿海、东北部、中部和西部等四个主要经济区域的生产率水平是否存在收敛的问题。我们发现企业进入和退出样本对生产率增长有着特殊的影响。在1998年至2005年间,这种进入和退出促进了中国工业生产率的增长,并且加快了内陆省份生产率对沿海地区的追赶。

|

| [39] |

Competition and corporate tax avoidance: Evidence from Chinese industrial firms [J].https://doi.org/10.1111/j.1468-0297.2009.02217.x URL [本文引用: 1] 摘要

This article investigates whether market competition enhances the incentives of Chinese industrial firms to avoid corporate income tax. We estimate the effects of competition on the relationship between firms reported accounting profits and their imputed profits based on the national income account. To cope with measurement errors and potential endogeneity, we use instrumental variables, exogenous policy shocks and other robustness analysis. We find robust and consistent evidence that firms in more competitive environments engage in more tax avoidance activities. Moreover, all else equal, firms in relatively disadvantageous positions demonstrate stronger incentives to avoid corporate income tax.

|

| [40] |

中国工业企业数据库的使用现状和潜在问题 [J].

在经验研究中,企业级的微观数据正受到越来越多的重视。中国工业企业数据库成为国内外学者研究中国企业行为和绩效的主要数据库之一。但是该数据库存在样本匹配混乱、变量大小异常、测度误差明显和变量定义模糊等严重问题,忽视这些问题可能会导致研究结论错误。本文介绍了该数据库的基本情况和使用现状,指出了该数据库存在的缺陷,并根据现有研究提出了改进建议。

Application status and potential problems in China industry business performance data .

在经验研究中,企业级的微观数据正受到越来越多的重视。中国工业企业数据库成为国内外学者研究中国企业行为和绩效的主要数据库之一。但是该数据库存在样本匹配混乱、变量大小异常、测度误差明显和变量定义模糊等严重问题,忽视这些问题可能会导致研究结论错误。本文介绍了该数据库的基本情况和使用现状,指出了该数据库存在的缺陷,并根据现有研究提出了改进建议。

|

| [41] |

出口与中国本土企业生产率——基于江苏制造业企业的实证分析 [J].

运用来自江苏省本土制造业企业微观数据,通过构建一个测度企业生产率的综合指标体系,利用联立方程计量方法,在解决企业出口和生产率之间内生性基础上,本文实证考察了企业出口与生产率之间的相互关系。研究表明,就测度企业生产率的全要素生产率(TFP)指标而言,出口虽然不是促进中国本土企业TFP增长的因素,TFP却是促进中国本土企业出口的因素;就作为测度企业生产率的资本生产率(S_K)要素生产率指标而言,S_K不仅促进了中国本土企业的出口,同时,出口又促进了中国本土企业的S_K的提升;就作为测度企业生产率的资本一劳动比率(K_L)单要素生产率指标而言,K_L不仅促进了中国本土企业的出口,而且,出口也促进了中国本土企业K—L的提升。更进一步,我们按企业规模和按产品特性分组划分,深入研究了企业出口与生产率的相互作用关系,发现不同规模与不同产品特性的企业出口与生产率关系,存在显著差异。这就为从更深入角度全面考察企业出口与生产率之间可能具有的复杂相互关系,提供了来自类似中国这样发展中大国的经验证据。

Export and productivity of local enterprises: An empirical analysis based on manufacturing enterprises in Jiangsu .

运用来自江苏省本土制造业企业微观数据,通过构建一个测度企业生产率的综合指标体系,利用联立方程计量方法,在解决企业出口和生产率之间内生性基础上,本文实证考察了企业出口与生产率之间的相互关系。研究表明,就测度企业生产率的全要素生产率(TFP)指标而言,出口虽然不是促进中国本土企业TFP增长的因素,TFP却是促进中国本土企业出口的因素;就作为测度企业生产率的资本生产率(S_K)要素生产率指标而言,S_K不仅促进了中国本土企业的出口,同时,出口又促进了中国本土企业的S_K的提升;就作为测度企业生产率的资本一劳动比率(K_L)单要素生产率指标而言,K_L不仅促进了中国本土企业的出口,而且,出口也促进了中国本土企业K—L的提升。更进一步,我们按企业规模和按产品特性分组划分,深入研究了企业出口与生产率的相互作用关系,发现不同规模与不同产品特性的企业出口与生产率关系,存在显著差异。这就为从更深入角度全面考察企业出口与生产率之间可能具有的复杂相互关系,提供了来自类似中国这样发展中大国的经验证据。

|

| [42] |

Competition and strategic information acquisition in credit markets [J].https://doi.org/10.2139/ssrn.302196 URL [本文引用: 1] 摘要

We investigate the interaction between banks' use of information acquisition as a strategic tool and their role in promoting the efficiency of credit markets when a bank's ability to gather information varies with its distance to the borrower. We show that banks acquire proprietary information both to soften lending competition and to extend their market share. As competition increases, investments in information acquisition fall, leading to lower interest rates but also to less efficient lending decisions. Consistent with the recent wave of bank acquisitions, we also find that merging for informational reasons with a competitor is an optimal response to industry consolidation.

|

| [43] |

Bank Relationships: A Review [J]. |

| [44] |

|

| [45] |

经济转型与中国省区产业结构趋同研究 [J].https://doi.org/10.3321/j.issn:0375-5444.2008.08.003 URL [本文引用: 1] 摘要

伴随经济转型的市场化、全球化和分权化过程是中国产业结构重组的重要力量。基于2004年第一次经济普查资料.深入探讨了中国制造业结构在不同产业层次的趋同问题。总体而言.多数省区与全国产业结构保持着较高的相似性,随着产业细分,产业结构相似系数呈明显下降趋势。东部沿海省区和全国相似程度最高,西部落后省份和全国相似性最低。资源密集型产业使省区结构与全国差异显著.全球化程度较高、附加值较高、产业联系较强的产业使区域产业结构趋同。统计结果显示.市场化进程有利于比较优势和区位优势的发挥,显著地促进了比较优势相似的省区产业结构趋同.而资源条件不同的省区结构差异化发展:参与经济全球化强化了比较优势对于产业区位的影响.相似国际市场需求以及区位和产业偏好相似的外资促使沿海省区产业结构趋同.也是沿海与内地省区产业结构显著不同的原因。地方分权导致省区市场严重分割.造成了一些省区产业结构趋同。

Economic transition and convergence of regional industrial structure in China .https://doi.org/10.3321/j.issn:0375-5444.2008.08.003 URL [本文引用: 1] 摘要

伴随经济转型的市场化、全球化和分权化过程是中国产业结构重组的重要力量。基于2004年第一次经济普查资料.深入探讨了中国制造业结构在不同产业层次的趋同问题。总体而言.多数省区与全国产业结构保持着较高的相似性,随着产业细分,产业结构相似系数呈明显下降趋势。东部沿海省区和全国相似程度最高,西部落后省份和全国相似性最低。资源密集型产业使省区结构与全国差异显著.全球化程度较高、附加值较高、产业联系较强的产业使区域产业结构趋同。统计结果显示.市场化进程有利于比较优势和区位优势的发挥,显著地促进了比较优势相似的省区产业结构趋同.而资源条件不同的省区结构差异化发展:参与经济全球化强化了比较优势对于产业区位的影响.相似国际市场需求以及区位和产业偏好相似的外资促使沿海省区产业结构趋同.也是沿海与内地省区产业结构显著不同的原因。地方分权导致省区市场严重分割.造成了一些省区产业结构趋同。

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}